Clearly the most important development during the period was the sudden and successful conclusion of US corporate tax reform. From an investment perspective, the largest benefits for US-domiciled companies are:

- A reduction in the headline tax rate for profitable corporations from 35% to 21%;

- An immediate, full deduction for new capex, creating a further tax shield for income; and,

- A territorial tax system, meaning that US companies are now free to repatriate foreign profits.

The fairly clear effects of these changes will be to increase the cash flow (and therefore the valuation) of profitable US companies; to increase domestic business demand; and quite possibly to catalyze a significant amount of M&A activity among American companies.

The slightly less clear effect is that the Fed governors now have a very strong case to continue increasing US interest rates, even absent further growth in inflation. Three rate increases are now priced into short-term US rates for 2018, but virtually none are priced in thereafter. It is unlikely for both of these levels to exist in harmony for long when combined with the massive fiscal stimulus (tax cuts) that have just been delivered. Medium and long-term US rates likely need to increase, particularly given the Fed balance sheet reduction that will continue through this year.

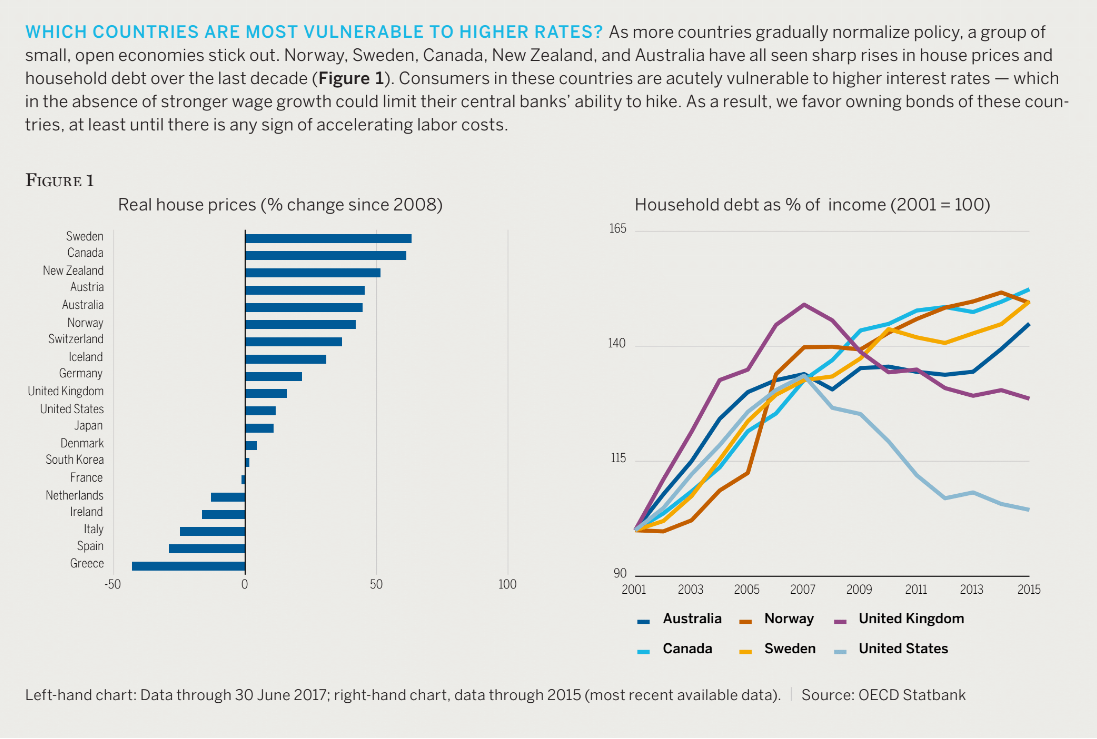

Rising interest rates, lower tax rates, and robust economic growth is a near-perfect combination for US bank stocks. Although the sector performed well through 2017, valuations still leave ample room for upside in the new environment. I would encourage reviewing the opportunities that we looked at in the sector back in Q1/Q2 2017. By contrast, Canadian bank stocks remain fully valued and generally do not have the same tailwinds (although CIBC’s purchase of Private Bancorp and RY’s purchase of City National now both look very timely). At the risk of sounds like Chicken Little, I will highlight that Toronto-area housing prices fell yet again last month, and in this rising rate environment, Canadian consumers remain the most indebted of all developed nations (see “OECD” attached).

Valuations in every other North American sector – except Energy – are now above historical averages. By itself, this is not a cause for alarm. It does mean that valuations warrant more attention this year than last; it also means that we should expect more volatility, after an almost perfectly tranquil 2017.