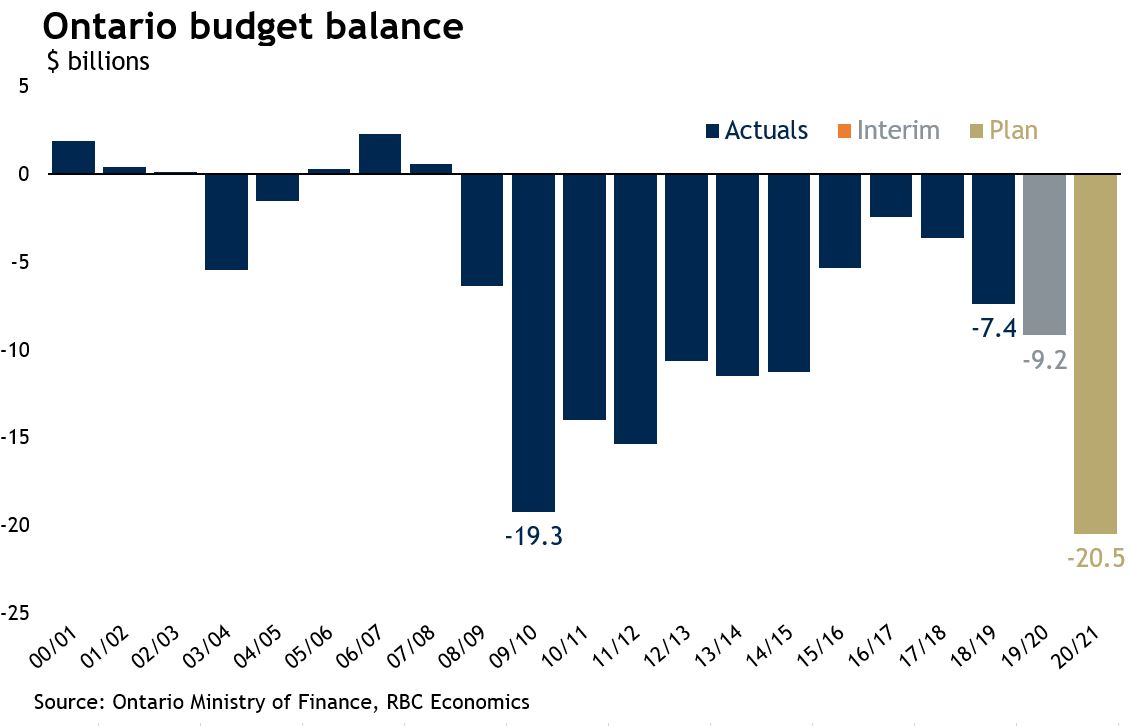

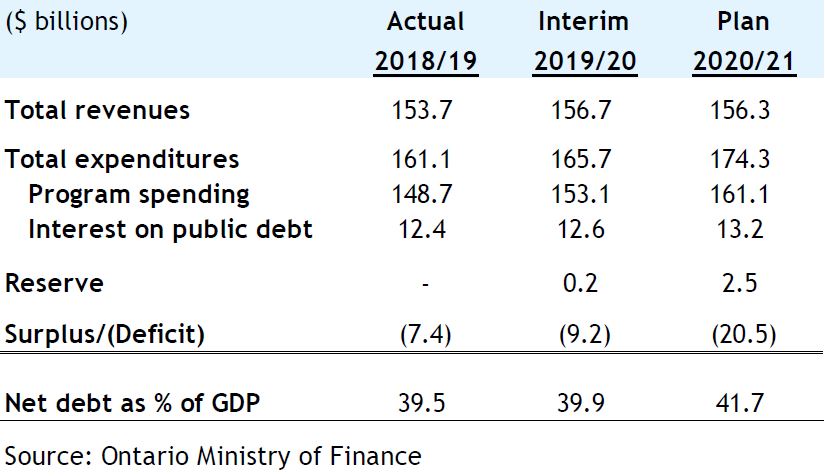

The plan was the main feature of the fiscal update presented by Finance Minister Rod Phillips. The update showed the budget deficit more than doubling to $20.5 billion (2.3% of GDP) in 2020-2021. The government estimates COVID-19 will drill a $5.8 billion hole into revenues and be the primary factor driving program expenses $9.1 billion above the previous baseline.

The fiscal framework assumes zero economic growth in 2020. This was set relative to private-sector forecasts a week ago and now appears overly optimistic in light of the sharp deterioration in the outlook since then. We updated our growth forecast for the province on March 25 and now expect a 2.1% contraction in 2020—pointing toward further downside risk to the province’s revenue projection.

The government handled the unprecedented degree of uncertainty by boosting its contingency reserve to a record-high $2.5 billion. It also increased its general contingency fund to $1.3 billion and set up a COVID-19 dedicated contingency fund of $1.0 billion. These prudence measures provide a sizable buffer. Whether it will be enough to protect against the effects of a prolonged period of social distancing and a drawn-out recession is an open question. Minister Phillips will give regular updates in the coming months as the situation evolves.

Ontario’s COVID-19 action plan is similar to the federal government’s $82 billion package announced last week (and boosted by $25 billion yesterday) in that it’s two-pronged. It has $7 billion in additional resources for the health care system and to provide direct support for people and businesses, and $10 billion in tax credits and deferrals largely to help businesses manage their cash flow.

The first $7 billion bucket is split with $3.3 billion going directly to support health care and $3.7 billion to fund a host of measures to support people and jobs during the crisis (e.g. emergency payments to people in need, funding to municipalities and other service providers responding to local needs, electricity cost relief, higher payments to seniors, student loan payment deferrals, and emergency assistance to Indigenous peoples and communities).

The Ontario government sees these initiatives a first step, and stands ready to do more if needed.

To fund the higher deficit and ongoing capital plan, the government is increasing its total long-term public borrowing from $36 billion in 2019-2020 (including $4.1 billion in pre-borrowing) to $43.6 billion in 2020-2021. This will be just shy of the $43.8 billion recorded at the depth of the Great Recession in 2008-2009. Net debt is projected to rise by $24 billion to $379 billion at the end of 2020-2021. As a percentage of GDP, net debt will climb from 39.9% in 2019-2020 to 41.7% 2020-2021.

There were no projections beyond next fiscal year. Minister Phillips indicated his government will present a full-blown budget (and multi-year fiscal plan) by November 15. Much can happen between now and then. We see plenty of downside risks that could worsen the sobering fiscal picture painted yesterday. Ontario isn’t alone – all provinces are facing dire prospects. The focus of governments must be to combat COVID-19, ensure the stability of our economy, and provide financial support to Canadian households and businesses in need. This is what Ontario’s action plan is all about. Worries about the province’s deficit or elevated debt will be the focus of another time when the health crisis is in the rear-view mirror.

Ontario’s fiscal plan

Robert Hogue is a member of the Macroeconomic and Regional Analysis Group, with RBC Economics. He is responsible for providing analysis and forecasts for the Canadian housing market and for the provincial economies. His publications include Housing Trends and Affordability, Provincial Outlook and provincial budget commentaries.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.