In November, Statistics Canada announced that the national savings rate was the lowest it has been since 2005. This is a worrying trend given an average retirement age in the low 60's and life expectancy going well into the 80's for both men and women. Saving for the future needs to be a priority for all of us and that was the impetus behind the changes to the Canada Pension Plan (CPP).

These changes, along with employment and retirement trends, highlight the importance of having and reviewing a financial plan with a special focus on retirement savings. Feel free to reach out to me directly here to discuss how these changes may impact your plan.

Here are the key highlights of the enhancements:

- The CPP retirement benefit will replace one third of your average work earnings received after 2019 (up from one quarter previously).

- The funding required to sustain the higher payout will come from increased employer and employee contributions.

- Step one of increasing contributions began January 1, 2019 with an increase of 15bps to both employer and employee contribution rates.

- Contribution rates will increase 4 more times over as many years to end up a full 2% higher than before the changes.

- Step two involves an additional contribution rate for income earned above the yearly maximum pensionable earnings and will take 2 years to implement beginning in 2024.

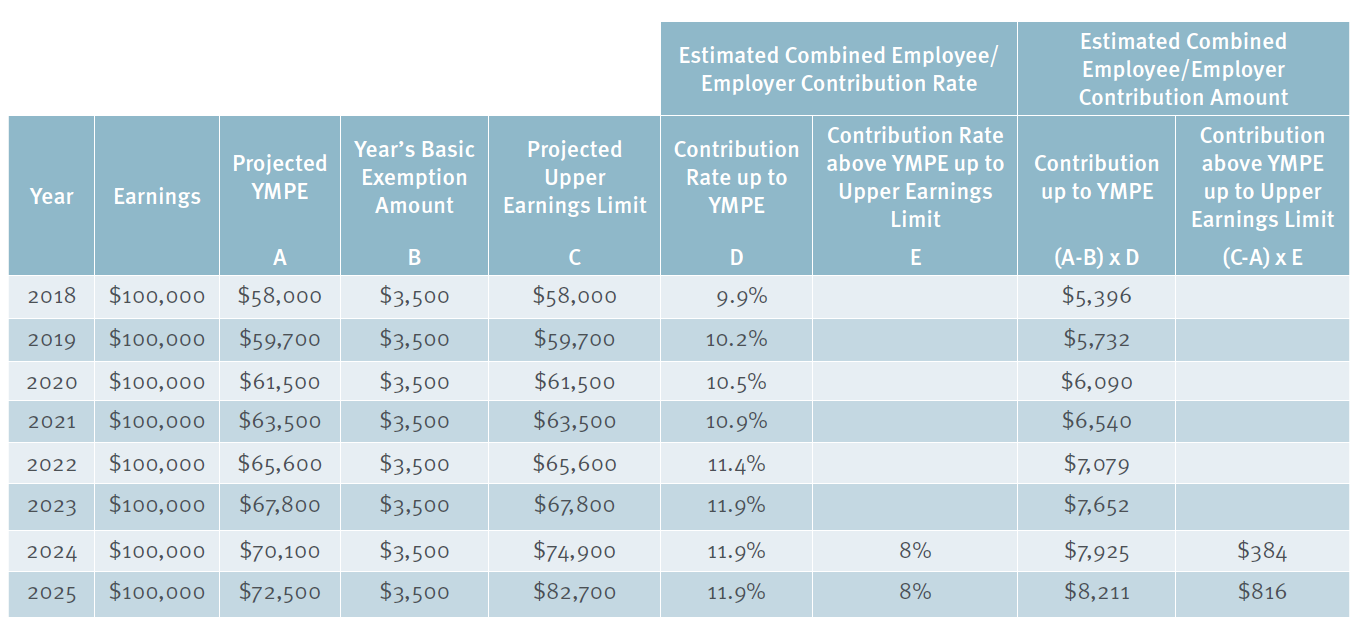

The following table shows the impact of the changes on a salary of $100,000 (source) .