“Life is 10% what happens to you, and 90% how you react to it.”

~ Charles R. Swindoll

Investors today can hardly be blamed for feeling whipsawed over the performance of equity and bond markets in the last two years, especially in Canada. Despite its late year-end rally, the S&P/TSX Composite Index ended up a moderate 8% for 2023 (following an 8% drop in 2022), which pales in comparison to the U.S.-based S&P 500 Index’s return of 24%. (note: all returns are price returns, as of December 29, 2023, and in Canadian and U.S dollars, respectively).

Of note, much of the gains for 2023 were achieved in the final weeks of the year, and belie the volatility of the market over the past 12 months, as investors grappled with decades-high interest rates and bond yields, and the uncertainty clouding the outlook for the economy and corporate earnings. And volatility and uncertainty have not just stalked markets this past year, but also in 2022, testing investors’ patience and even their commitment to well-structured and risk-profile-appropriate portfolios.

While equity markets rallied to end the year, and bond yields have come down sharply (and seem poised to continue to fall), economic uncertainty remains an issue for 2024. While investors have celebrated the expectation that central banks will cut interest rates this year, likely in the spring or summer, this may be due more to a slowing economy than just a defeat of inflation pressures. That could mean that 2024 will be another tricky year for consumers and businesses, but with hope on the horizon as the year progresses.

However, volatility and uncertainty are almost always present when investing, and they can rightfully be seen as the short-term “toll” the market takes on investors to deliver long-term gains. So while you can’t control the markets, you can control how you react to them. What’s more, you can also consider strategies to improve your financial situation – even when markets are volatile.

Here are six ideas that can help:

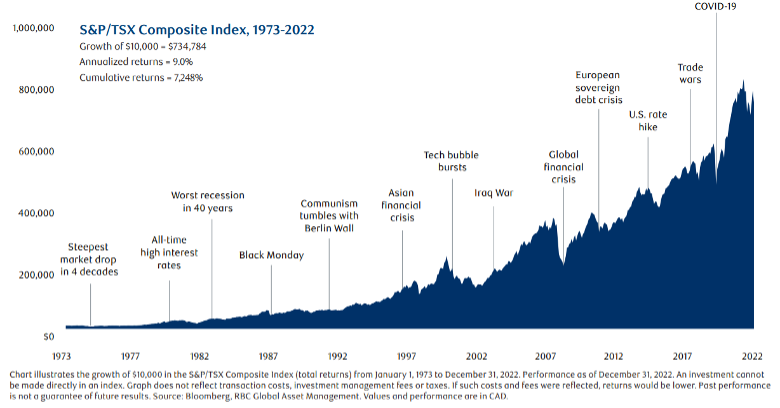

1. Don’t panic – time and history are on your side

Unfortunately, there are times when markets do not deliver the returns we’d like. But looking at the history of markets, periods like the ones we’ve experienced over the last few years are not unusual – nor are they something to fear or change our course over. In fact, downturns for investment markets are historically excellent opportunities to take advantage of lower asset prices, while waiting for more normal conditions to return to benefit from their rebound. While there are always reasons not to invest, looking at the following chart shows why crises can really be opportunities in disguise:

2. Financial planning: Review your plan and your immediate cash-flow needs

A written financial plan or retirement projection can help to put market volatility into perspective. It’s important to know the options available if your plan is off track. If you are concerned you may not meet your long-term objectives, consider any actions you can take in order to meet your goals. For example, if you are approaching retirement, can you continue working an additional few years? Can you reduce your retirement expenses? Can you save more now?

3. Investment planning: Cash isn’t “king” in a world of falling interest rates

Certainly “cash” – e.g., High-Interest Savings Accounts, money-market funds, short-term GICs, etc. – can be a smart place to park your money in the short term, and especially when interest rates are at 20-plus year highs and you are looking to hide out during volatile times in markets. But don’t be fooled. If you are a long-term investor with a proper plan that reflects your up-to-date goals and investment risk profile, parking your money in cash may mean you miss out on critically important returns. Just missing a handful of up days in the markets can have an extremely negative effect on your wealth-building efforts:

Source: Morningstar, RBC GAM. Data reflects price returns of the S&P/TSX Composite Index and in Canadian currency. Data as of December 15, 2023. Returns greater than 1 year are annualized. Note that an investment cannot be made directly into an index. The chart does not reflect transaction costs, investment management fees nor taxes. If such costs were reflected, returns would be lower. Past performance is not a guarantee of future results.

4. Tax planning: Convert capital losses into tax advantages

By selling investments that have gone down in value, you can turn “lemons” into “lemonade” – at least from a tax perspective. Here’s how. First, consider whether you have any investments in your non-registered account that are worth less than what you paid for them. Do they still meet your investment goals? If not, it can make sense to consider selling them, in order realize the capital loss. That’s because you can apply the capital loss against any taxable capital gains realized in the current year (or any of the previous three years). This can reduce your taxable capital gains. We can help you identify which investments to consider selling. You should also speak to a qualified tax advisor to ensure this strategy makes sense for you, given your individual situation.

As well, consider making your RRSP and TFSA contributions (2024 TFSA contribution limit: $7,000) as early in the new year as possible, allowing you to maximize the benefit from the tax-sheltered compounding of returns, while helping to ensure that other competing priorities don’t arise and draw away these important investments that are critical to you achieving your long-term goals.

Reminder: The 2023 tax-year cut-off for RRSP contributions is February 29, 2024 (yes, it’s a leap year).

5. Charitable giving: Giving is its own reward, but giving “in kind” is smart planning

Do you have securities like stocks that have appreciated in value? Are you considering selling them and donating the proceeds to charity? To maximize your gift, consider donating them in-kind instead. If you give actual securities in-kind (i.e., transfer directly to the charity), the donation is assessed at the fair market value of those in-kind assets – AND you do not pay the usual capital gains tax. If you sell those assets and donate the proceeds in cash, you will have to pay taxes on the capital gains AND you will consequently reduce the net donation proportionally. Please speak to a qualified tax advisor to determine if this strategy makes sense for you and your circumstances.

6. Business management: When markets are cold, consider an estate freeze

If the value of your business shares has recently declined, consider an estate freeze or refreeze – particularly if your company is expected to grow in value once market conditions rebound. An estate freeze fixes the value of the asset, such as shares of a corporation, for the owner until the time of their death, allowing them to anticipate their tax liability arising when they pass on. In short, an estate freeze may help limit the value of the company that will be taxed in your hands upon death, and shifts future growth to your successors or other family members. Please speak to a qualified tax advisor to determine if this strategy makes sense for you and your circumstances.

We can help

Volatile markets and uncertain economic conditions are tough on investors, often straining their patience, and tempting them to veer off plan and make poor long-term decisions based on emotions rather than reason. The six points above are not exhaustive. Your Investment Counsellor can help figure out how to turn the lemons the market and economy are handing you today into the advice and options that can pay off for years to come.

Past performance is not indicative of future results. Counsellor Quarterly has been prepared for use by RBC Phillips, Hager & North Investment Counsel Inc. (RBC PH&N IC). The information in this document is based on data that we believe is accurate, but we do not represent that it is accurate or complete and it should not be relied upon as such. Persons or publications quoted do not necessarily represent the corporate opinion of RBC PH&N IC. This information is not investment advice and should only be used in conjunction with a discussion with your RBC PH&N IC Investment Counsellor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest information available. Neither RBC PH&N IC, nor any of its affiliates, nor any other person accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. This document is for information purposes only and should not be construed as offering tax or legal advice. Individuals should consult with qualified tax and legal advisors before taking any action based upon the information contained in this document. Some of the products or services mentioned may not be available from RBC PH&N IC; however, they may be offered through RBC partners. Contact your Investment Counsellor if you would like a referral to one of our RBC partners that offers the products or services discussed. RBC PH&N IC, RBC Global Asset Management Inc., RBC Private Counsel (USA) Inc., Royal Trust Corporation of Canada, The Royal Trust Company, RBC Dominion Securities Inc. and Royal Bank of Canada are all separate corporate entities that are affiliated. Members of the RBC Wealth Management Services Team are employees of RBC Dominion Securities Inc. RBC PH&N IC is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada. RBC, RBC Wealth Management and RBC Dominion Securities are registered trademarks of Royal Bank of Canada. Used under licence. © RBC Phillips, Hager & North Investment Counsel Inc. 2024. All rights reserved.