This report is part of the “New normal, new opportunities” series, in which we examine secular trends in a post-COVID-19 world. The series will cover a range of themes that are emerging as a result of social distancing, the work-from-home imperative, health care developments, corporate implications, and broader societal change. We believe identifying these trends and understanding their investment implications will be critical to navigating the road ahead. Additional reports will be released over the next few months.

The pandemic has provided a unique glimpse into a world where society has become hyper-reliant on digital infrastructure to communicate, transfer value, and conduct commerce. Though trends in both individual and corporate digital transformations were firmly in place prior to COVID-19, the pandemic has forced companies to cross the digital threshold with far more urgency. This report explores the specific impact of COVID-19 on digital payments as quarantine measures alongside hygiene concerns have accelerated the pre-existing secular shift.

Pandemic driving increased adoption

Though the transition away from cash towards digital payments was firmly in place entering 2020, the COVID-19 pandemic has accelerated this shift as quarantine measures forced consumers to transact more online for everyday necessities while brick-and-mortar businesses encouraged the use of credit cards over cash given hygiene concerns. In our view, these COVID-19-related behaviours combined with the drivers that were formerly in place (e.g., adoption of digital wallets, higher smartphone penetration, and increased digital infrastructure investments by merchants) have made what was already an attractive secular growth theme far more robust.

We would highlight that the recent launch of 5G-capable smartphones will further accelerate digital payments adoption as this new communications standard will allow networks to handle digital transactions at scale given significantly reduced latency (the time it takes for a connected device to make a request from a server and get a response).

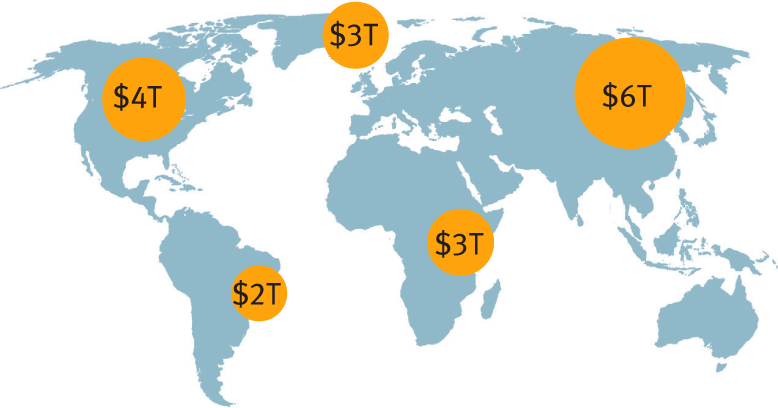

Global breakdown of cash and checks ($ trillion)

Source - Visa Inc.

Large global market opportunity across multiple payment flows

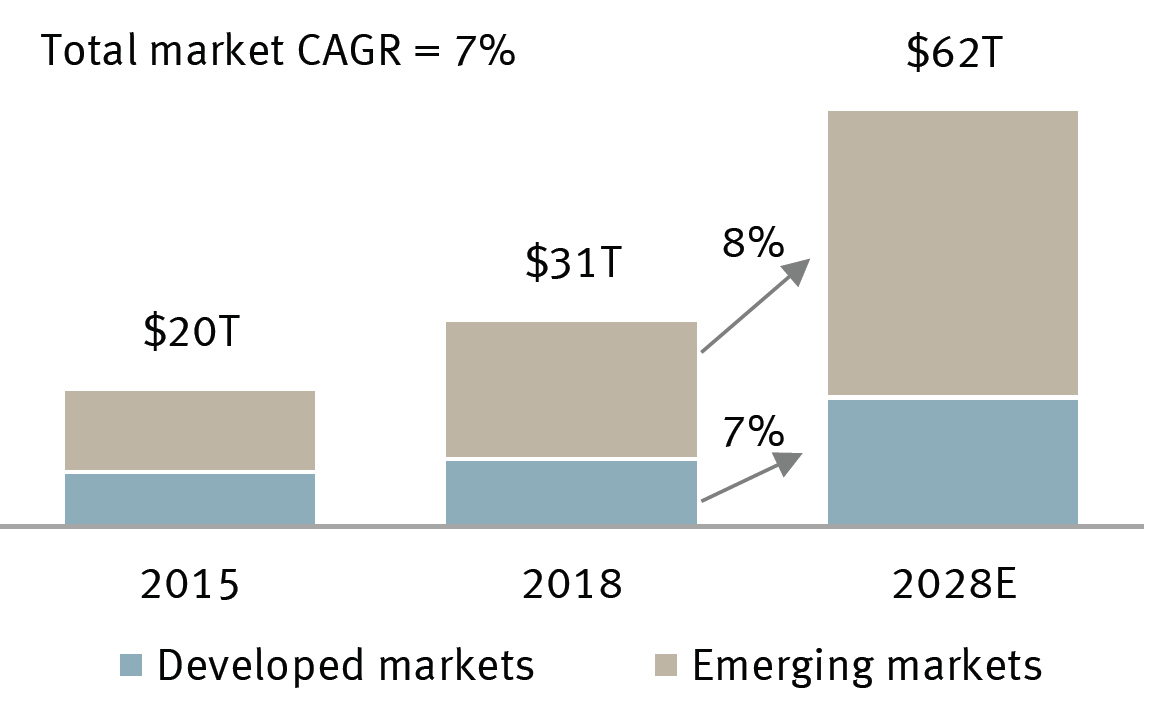

According to MasterCard Inc. (MA), the long-term global opportunity across multiple payment flows—including personal consumption expenditures (PCE), peer-to-peer (P2P), business-to-business (B2B), and business-to-consumer (B2C) transactions—stands at $235 trillion, and we believe it is ripe for further disruption. According to RBC Capital Markets, approximately $18 trillion of global PCE was still accounted for by cash and checks. Based on data from the Nilson Report, RBC Capital Markets estimates that PCE growth combined with the secular shift away from these paper-based transactions will generate a seven percent compound annual growth rate in purchase volume on cards from 2018–2028.

Global card payment volume

Source - The Nilson Report, RBC Capital Markets estimates

The P2P market continues to be propelled by the increasing ubiquity of digital wallets that have allowed individuals to transfer value through digital applications. Meanwhile, the motivation driving the B2C potential has been the speed of transactions combined with the security benefits as physical cash is no longer required to be held on premises. Finally, as it relates to the B2B possibility, the majority of accounts payable globally are still processed manually and paid by certified checks, which not only expose transactions to clerical errors but is also time consuming as these payments typically require several weeks to process.

In contrast to PCE, digital penetration rates in B2B and B2C remain significantly lower and represent a large proportion of the $235 trillion global opportunity. Ultimately, the prospect for digitizing the global payments market remains substantial, and we continue to be constructive on the longer-term growth trajectory of the industry.

This article was initially published on 8/3/20.

Non-U.S. Analyst Disclosure: Jim Allworth, an employee of RBC Wealth Management USA’s foreign affiliate RBC Dominion Securities Inc. contributed to the preparation of this publication. This individual is not registered with or qualified as a research analyst with the U.S. Financial Industry Regulatory Authority (“FINRA”) and, since he is not an associated person of RBC Wealth Management, may not be subject to FINRA Rule 2241 governing communications with subject companies, the making of public appearances, and the trading of securities in accounts held by research analysts.

In Quebec, financial planning services are provided by RBC Wealth Management Financial Services Inc. which is licensed as a financial services firm in that province. In the rest of Canada, financial planning services are available through RBC Dominion Securities Inc.