Investors have sold off the bank group in a very aggressive fashion during the crisis, with the TSX/S&P Commercial Banks Index down approximately 30%

from its February high. Low interest rates, slowing economic activity, the collapse in energy prices, and credit concerns are all top of mind and driving investor concern around dividend sustainability. While nothing is ever certain, especially in such uncertain times, below we look at key factors investors should consider when assessing the dividend outlook for the Canadian banks.

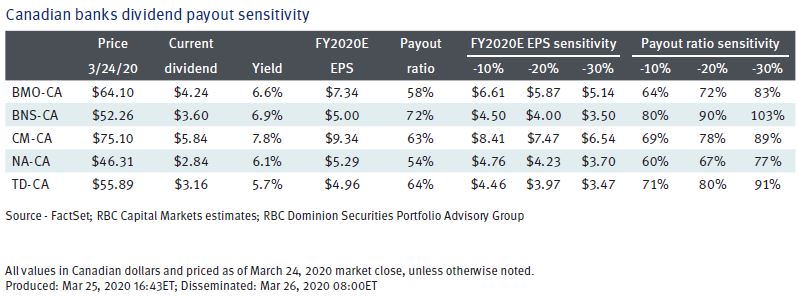

Payout ratios – Sensitivity to changes in earnings estimates

The Big Six Canadian banks have dividend policies that roughly target a payout ratio of 40%–50% of earnings over the medium term, which allows the banks to maintain a steady dividend stream despite potential short-term volatility in earnings. In light of the quick and dramatic change in the economic outlook, consensus estimates for the banks have come down and could continue to move lower as the concerns mentioned above potentially intensify. In the table below, we present a very simplistic analysis of what the payout ratios (dividends divided by earnings) for the major Canadian banks (excluding RY) would look like if RBC Capital Markets’ (RBCCM) fiscal year 2020 (FY2020) earnings estimates were lowered by 10%, 20%, and 30% from current levels. We note that this scenario analysis is in addition to the 23% average reduction in RBCCM’s FY2020 earnings estimates published on March 23,

which reflect a Canadian recession and corresponding increases in credit provisions.

An additional 30% decline in earnings estimates from current levels would be required to get the Canadian banks into the approximate 80%–100% payout range.

While we are not ruling out a further 30% decline in earnings estimates, a more plausible 10%–20% decline would place payout ratios in the 70%–80% range on average.

The banks have operated at payout ratios in that range before—most recently during the 2008–09 Global Financial Crisis (GFC). In our view, if the range is reached again, the banks will be as well-equipped to handle this scenario as they have ever been given our belief that the banks are better managed, more diversified, and better capitalized than ever.

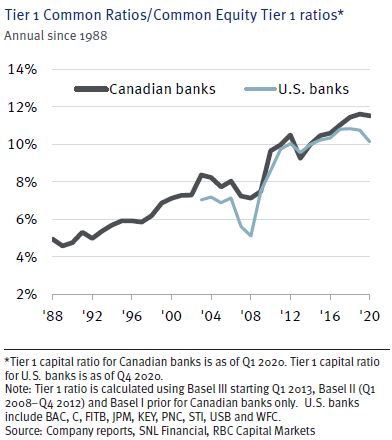

Capital levels – Banks are very well capitalized

One of the key outcomes of the GFC was the acceptance by investors that the banks will now have to operate under a new normal, where higher levels of capital are simply a cost of doing business in the post-financial crisis age. The chart at the right shows the Common Equity Tier 1 (CET1) ratio (a measure of a bank’s capital relative to its assets) of the bank group going back to 1988. The ratio has increased to nearly 12% at present from sub-8% during the GFC. This means the banks are significantly more capitalized to handle economic shocks than they were during the GFC. This is key, as having an adequate capital buffer in place should reduce the probability of a bank having to pause or reduce its dividend in times of stress.

As an added level of capital flexibility, Ottawa announced last week that it will loosen the capital requirements for the banks. The Office of the Superintendent of Financial Institutions (OSFI) has lowered the domestic stability buffer (DSB) banks must maintain to 1% from 2.25%. Now, to be very clear, the lowering of this buffer is to encourage lending, and OSFI expects the banks to refrain from using the added capacity to increase dividends or buy back shares. Nevertheless, the added capacity does further support the argument there will be a sufficient level of available capital to support current dividends in a temporarily stressed scenario.

All that said, investors should be aware that, while we believe it is highly unlikely, a pause in the distribution of dividends could occur. We point to a report published by the Bank of Canada (BoC) last year titled, “Assessing the Resilience of the Canadian Banking System”. In it, the BoC stress tested the Big Six under very dire assumptions (8% decline in real GDP, seven consecutive quarters of negative growth, 12.6% peak unemployment rate, and a 41% decline in housing prices). The result was that aggregate capital levels would erode over their three-year stressed period, but capital levels would

remain well above the regulatory minimum (4.5%). However, early in the second year of the stressed scenario, the banks breach the capital conservation

buffer (CCB) threshold of 8%. This means banks would face automatic restrictions on dividend distributions in order to reduce the rate of capital depletion. Again, this is the modeled result of a very severe downside scenario that is beyond what we currently contemplate.

Signaling – Cutting dividend is option of last resort

Based on past precedent (1990 recession, dot-com bust in 2000, GFC in 2008–09, and the oil price collapse in 2014–16), cutting the dividend is the last capital strengthening avenue banks will consider, as bank boards would have to be convinced that medium-term earnings power could not support the dividend. As such, we think a cut in a major bank dividend would signal a very draconian outlook for the Canadian economy. Given we ultimately expect the impacts of COVID-19 to be transitory, and given the payout ratio scenarios in the table on page 1, we are hard pressed at this time to believe the boards of the major banks will be forced to take such dire action. Also, remember that a large portion of the shareholder base of the Canadian banks

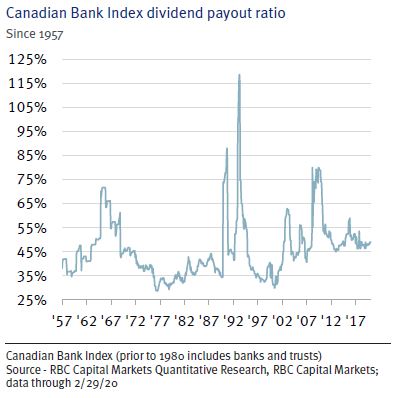

is retail investors who own bank shares for the dividend yield. We note that within the Big Six there have only been two dividend cuts since 1990, both from National Bank, the smallest of the Big Six, in 1992–93. However, it is also important to point out that history alone should not lull investors into a false sense of security. Whether the banks will cut their dividends or not, should be based on the facts as they are today. In our view, the banks are in as strong a position as they have ever been, thanks in part to the lessons learned from the GFC. While in our base case, we do not expect the banks to cut their dividends on the back of COVID-19 and the oil price decline, a scenario where they increase dividends on their every-other-quarter schedule (except TD that reviews its dividend policy annually), may not happen for the remainder 2020. Recall, as part of OSFI’s lowering of the DSB mentioned earlier, the banks are now precluded from increasing their dividends or buying back shares, until further notice by the regulator.