Welcome back to the blog!

In addition to working with clients on wealth planning goals and objectives, I write a quarterly blog on tax tips and tidbits. In this edition, I’ll summarize the real estate tax changes introduced in BC over the last few years in an attempt to cool the market and address severe affordability issues.

So let's talk real estate and taxes

It is hard to go anywhere in Vancouver without hearing people talk about the sky-high real estate prices and the state of the market.

Most of you are likely aware of some of the municipal and provincial legislation introduced to address this issue, including:

- Foreign buyer’s tax (FBT), applicable to purchases by a foreign entity in specified regions of BC.

- Speculation and vacancy tax (SVT), applicable on vacant homes in specified regions of BC.

- Empty homes tax (EHT), applicable on vacant homes within the city of Vancouver.

- Increased school tax (STR), applicable on homes in BC worth more than $3 million.

- Increased property transfer tax (PTT) on homes in BC worth more than $3 million.

Further, new mortgage stress rules were recently introduced that in effect reduce the amount that can be borrowed.

Now, if you prefer a bit more detail over the to the previous point summary, continue below.

Foreign buyer's tax

A foreign entity is required to pay an additional property transfer tax on certain residential property transfers. In 2018, the FBT increased to 20 percent and it was extended to properties beyond Metro Vancouver including the following regions:

- Capital Regional District.

- Regional District of Central Okanagan.

- Fraser Valley Regional District.

- Regional District of Nanaimo.

A foreign entity includes a foreign national, which is typically an individual that is not a Canadian citizen or permanent resident, foreign corporations and taxable trustees.

If you already own a home, the FBT shouldn’t be of impact, except perhaps to a sale price.

Speculation and vacancy tax

In late 2018, retroactive legislation was enacted aimed at real estate speculators who leave homes vacant and do not pay tax in BC. The SVT applies to unoccupied residential properties located in the following regions:

- Metro Vancouver Regional District (excludes Bowen Island and Lions Bay).

- Capital Regional District (excludes some Gulf Islands).

- Kelowna, West Kelowna, Abbotsford, Chilliwack, Mission Nanaimo + Lantzville.

In 2019 and subsequent years, the SVT rates on the assessed value are as follows:

- 2 percent for foreign owners and members of a satellite family.

- 0.5 percent for Canadian citizens or permanent residents who are not members of a satellite family.

A satellite family includes people who declare less than half of their household income on Canadian income tax returns.

Now, although there are some exclusions and tax credits available, I suggest a careful review when completing the required annual declaration to assess if the SVT applies.

Increased school tax

In 2019, the additional school tax applies on the value of residential real estate in BC in excess of $3 million as follows:

- 0.2 percent on the residential portion assessed between $3 and $4 million.

- 0.4 percent on the residential portion assessed over $4 million.

Interestingly, the tax has nothing to do with education funding as it is going into the coffers as general revenue, meaning it can be spent on anything going forward

If you are cash flow crunched, consider deferring your property taxes if you are 55+ as a way to defer the whole payment.

Empty homes tax

In 2017, Vancouver introduced the EHT at 1 percent annually of the assessed value of unoccupied residential property.

The objective of the tax is to return empty or under-utilized properties to use as long-term rental homes. A few exclusions include:

- A principal residence (typically where you live and receive mail). of the owner, family member or friend.

- A property rented at least 6 months of the year in periods of 30+ consecutive days.

A property status declaration must be made annually or a property will be deemed to be vacant with applicable penalties for failure to file or false declarations.

In contrast to the increased school tax, revenue from the EHT will be reinvested into affordable housing initiatives.

BC property transfer tax

I’ve saved the simplest for last, the payment of property transfer tax, which is generally required with the change in ownership of property and is assessed as follows:

- 1 percent on the first $200,000.

- 2 percent on the amount between $200,000 and $2 million.

- 3 percent on the amount between $2 and $3 million.

In 2018, the effective rate increased from 3 to 5 percent on residential property value in excess of $3 million.

So where do we go from here?

So, what’s going to happen to the housing market as we look forward into the future?

In the last 12 to 18 months, we’ve seen inventories rise, sales decrease, and prices pull back, however, the question is difficult. There are many different housing markets within Vancouver, including single family homes, townhouses and condos, and each is impacted differently. It is safe to assume that housing affordability will continue to remain a serious problem a year from now.

In light of the legislative changes, it is important to review and assess the impact of these initiatives on the costs of ownership of existing property as well as the applicability to the purchase of future properties.

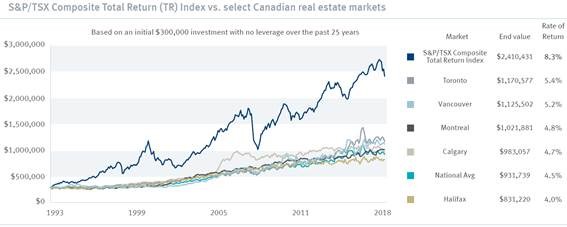

In BC, real estate has been a good investment, however, it might surprise some that returns have trailed the stock market as illustrated below.

I can be reached at craig.dale@rbc.com or 604.981.6681.

The blog may contain several strategies, not all of which will apply to your particular financial circumstances. The information in this blog is not intended to provide legal, tax or insurance advice. To ensure that your own circumstances have been property considered and that action is taken based on the latest information available, you should obtain specific professional advice before acting on any information in this blog.

This information is not investment advice and should be used only in conjunction with a discussion with your RBC Dominion Securities Inc. Investment Advisor. This will ensure that your own circumstances have been considered properly and that action is taken on the latest available information. The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / TM Trademark(s) of Royal Bank of Canada. Used under license. © 2019 RBC Dominion Securities Inc. All rights reserved.