Life is often about making choices, choices that require us to give up one thing to attain another. Often, our choices are clear ones for which we know the “right” versus the “wrong” decision. Others are dictated by our budget or means, or by simple preference, appetite or inclination. Financial and investment choices can often be more difficult given their impact on achieving our long-term goals, especially without proper advice or a clear understanding of the implications of one choice over another.

Fortunately, when it comes to saving, you don't have to choose between a Registered Retirement Savings Plan (RRSP) and a Tax-Free Savings Account (TFSA). They each have unique characteristics, advantages and rules. The smartest wealth plans often use both accounts to achieve different or even the same goals. Think of them as two different tools in your savings toolkit, each with their own unique strengths that can work beautifully together.

Let's break down what makes each account type special, and how they can team up to help grow your savings.

RRSPs and TFSAs: Understanding the basics

Both RRSPs and TFSAs are government-registered accounts, sometimes referred to as “tax-sheltered accounts”, that help Canadians save money through important tax advantages.

The key difference between them is when you get your tax break. With an RRSP, you get a tax deduction today, and your savings grow tax-free until you withdraw them.1 With a TFSA, your money grows tax-free and can be taken out completely tax-free, whenever and forever, but you don’t get a tax deduction when contributing to it.2

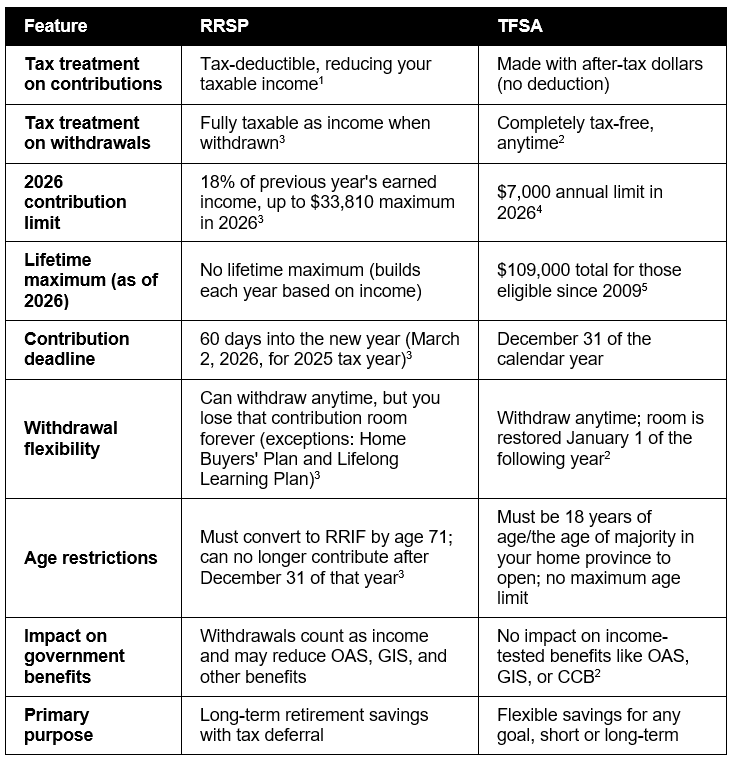

RRSPs and TFSAs: A side-by-side comparison

Their unique advantages, your unique goals: how they can work for you

So, how do you decide which account to use? If you are in your peak earning years, an RRSP can be your best friend. The tax deduction provides meaningful relief, and later, you may pay less tax when you take the money out in retirement, and might benefit from the lower rate on those savings.

At the same time, a TFSA offers incredible flexibility. Because you can access your money tax-free,2 it can be a great choice for an emergency fund, saving for a down payment, or adding to your retirement income without affecting income-tested government benefits.

This is why you don't have to pick just one. Many Canadians save smart by using both accounts. Your RRSP is like a powerful workhorse, pulling your savings toward retirement. Your TFSA is like a financial Swiss Army knife, giving you the right tool for any situation.

Both accounts let you carry forward unused room from year to year, so you never lose the chance to catch up when your finances allow. For the 2025 tax year, you can contribute to your RRSP until March 2, 2026.3

We can help

Every investor's situation is unique, so a personalized strategy is the key to making these accounts work for you. Your RBC Dominion Securities Investment Advisor can review your income, goals, timeline, and tax situation to build a plan that takes full advantage of both RRSPs and TFSAs, including how best use your TFSA, and your RRSP contributions, today.

Contact us to establish or review your plan and see your "better together" strategy in action.

Sources

- RBC Wealth Management. “Strategies to take control of your wealth.” https://www.rbcwealthmanagement.com/en-ca/insights/worried-about-higher-interest-rates-and-taxes-strategies-to-take-back-control-of-your-wealth

- RBC Royal Bank. "TFSA Rules and Contribution Limits." https://www.rbcroyalbank.com/investments/tfsa-rules-contribution-limits.html?_gl=1*ol0w5a*_up*MQ..*_ga*ODA0NDIxNDQ5LjE3NzA0MTIxNDQ.*_ga_89NPCTDXQR*czE3NzA0MTIxNDQkbzEkZzAkdDE3NzA0MTIxNDQkajYwJGwwJGgw*_ga_22PRMSS*czE3NzA0MTIxNDQkbzEkZzAkdDE3NzA0MTIxNDQkajYwJGwwJGgxNzc5Mjc5MDk1

- RBC Royal Bank. "RRSP Rules and Contribution Limits." https://www.rbcroyalbank.com/investments/rrsp-rules-contribution-limits.html

- Government of Canada. “Calculate your TFSA contribution room.” https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account/contributing/calculate-room.html

- RBC Royal Bank. “How much can I contribute to my TFSA.” https://www6.royalbank.com/en/di/hubs/investing-academy/chapter/how-much-can-i-contribute-to-my-tfsa/ki58km3m/ki58km3u

This publication is not intended as nor does it constitute tax or legal advice. Readers should consult their own lawyer, accountant or other professional advisor when planning to implement a strategy.

The content in this article is for information purposes only and does not constitute tax or legal advice. It is imperative that you obtain professional advice from qualified tax and legal advisors before acting on any of the information in this article. This will ensure that your own circumstances are properly considered and that action is taken based on the most current legislation

RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member-Canadian Investor Protection Fund. RBC Dominion Securities Inc. is a member company of RBC Wealth Management, a business segment of Royal Bank of Canada. ® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Dominion Securities Inc. (2026). All rights reserved.