Highlights

-

Headline risks and geopolitical events were prevalent throughout 2025, leading to significant market volatility. The significant progress in artificial intelligence (AI) emerged as the dominant narrative, minimizing the impact of initial tariff fears

-

Returns in 2025 were concentrated within a narrow set of names, sectors, and investment styles. Active management faced challenges. We anticipate that this year will mark a return to fundamental analysis, with individual valuations becoming a more critical determinant of equity performance

-

While monetary policy served as a primary economic catalyst throughout 2024 and 2025, its influence is beginning to moderate. Consequently, government deficit spending and debt financing are expected to emerge as the primary drivers of economic stimulus. We maintain a positive outlook for risk assets and the broader economy, and expect strong corporate earnings growth and a transformative impact from the ongoing expansion and adoption of AI

2025: Year-in-Review

2025 was an extraordinary and, at times, disorienting year for investors.

Markets were fast moving, shaped less by traditional economic factors, and more by an unusual convergence of geopolitical tension, increased fiscal activity, and trade policy uncertainty across major economies.

Against this backdrop, fundamental investors were challenged to navigate rapidly shifting narratives, inconsistent data signals, and elevated headline risk – often with limited historical precedent.

The following events and themes were among the most influential drivers of uncertainty, sentiment, and market volatility during the year.

2025 Events and Themes:

-

Repeated threats to Canadian sovereignty by its closest ally

-

Political instability in Canada (Prime Minister Trudeau steps down, Parliament prorogued)

-

Weakening economic fundamentals in Canada (housing, immigration, trade)

-

Global trade war (U.S. vs. Canada/Mexico, and U.S. vs. rest of the world)

-

Geopolitical tensions (U.S., China, Ukraine, Iran, Venezuela, Greenland)

-

Global fiscal spending (U.S. Big Beautiful Bill, Germany stimulus package)

-

Growing fiscal imbalances and rising government debt levels

-

U.S. government shutdown (including lack of U.S. economic data)

-

AI boom (capital spending, easing of government policy, corporate adoption, substantial driver of U.S. and global economic growth)

-

U.S. Federal Reserve independence uncertainty

-

Widening wealth gap (K-Shaped economy)

Despite a highly uncertain and rapidly evolving landscape, economic growth and corporate earnings significantly exceeded consensus expectations in 2025. Estimates suggest 2025 S&P 500 year-over-year earnings growth will register a low double digit percentage increase, while the U.S. economy experienced GDP growth expansion of 2.3% on an annual basis as of September 2025.

Broad based fiscal initiatives and AI related capital spending offset much of the early effect of raised tariff rates. In addition, corporate CEOs prioritized cost management and productivity enhancement by implementing hiring freezes across its workforce, as well as accelerating the adoption of artificial intelligence.

In contrast to 2024 and prior years, active investment managers materially underperformed their benchmarks. Robust equity market returns in 2025 were driven by narrow market leadership and geopolitical shocks, Canadian equity performance was unexpectedly led by gold companies and banks, while U.S. gains were largely propelled by AI and large-cap technology leaders.

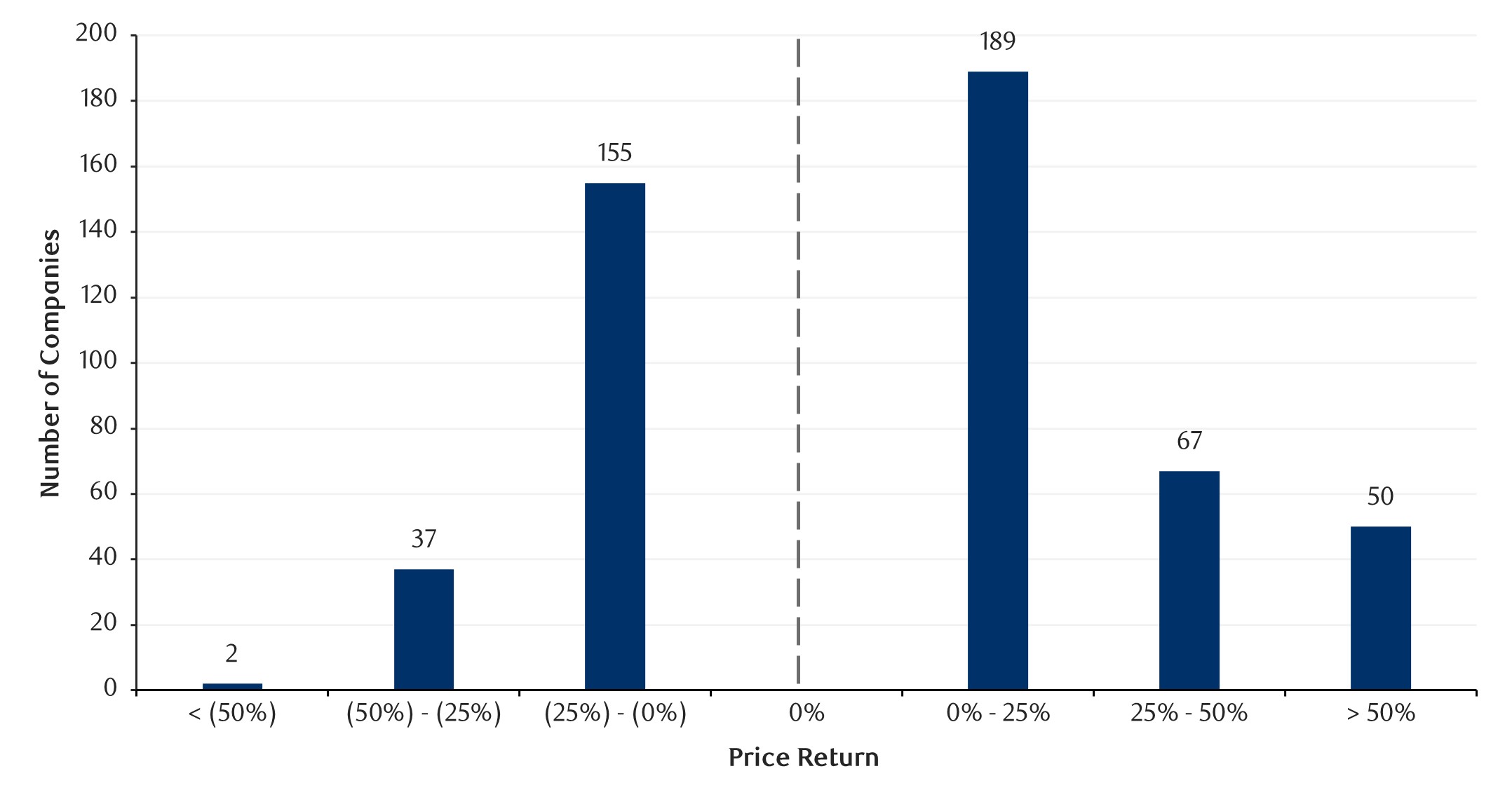

Despite strong headline index performance, many underlying companies did not produce positive returns. Approximately 40% of S&P 500 companies declined in price in 2025 – indicating a very bifurcated and polarized market. Figure 1 presents the extremely wide range of outcomes across America’s largest companies.

Figure 1: S&P500 Price Performance by Company (2025 Calendar Year)

Source: Ascendant Wealth Partners, FactSet. Price return data presented for calendar year 2025 (as of December 31st, 2025).

2026: Outlook

We maintain a favourable view of equities and risk assets. Our positive view is predicated by the following factors: continued fiscal spending, supportive monetary conditions, strong corporate earnings growth, and the ongoing expansion and adoption of AI:

1. A More Resilient Global Economy / Driven by Government Fiscal Stimulus

-

Positive economic momentum is underway – underpinned by fiscal spending (across developed and emerging market governments)

-

The global economy is expected to gain fresh momentum into 2026, propelled by upward growth revisions in the U.S., Eurozone and Emerging Markets. Broad-based fiscal stimulus across all major economies, alongside technology-driven capital expenditures, offers vital tailwinds

-

We have only seen the early impact of the Big Beautiful Bill on economic and investment activity (including individual and corporate tax cuts, increased investment in defence and technology initiatives, incentives for reshoring manufacturing, the reinstatement of 100% bonus depreciation for qualifying property, etc.). More of an impact expected in 2026 and 2027

-

Long-term wealth trends have the U.S. economy increasingly reliant on spending by upper-income households. A weakening job market and tariff cost pass-throughs may squeeze disposable incomes and spending at the margin

-

Emerging Markets are increasingly viewed as a compelling alternative to U.S. equities, which appear overextended following years of large-cap technology leadership. A stabilizing or depreciating U.S. Dollar is expected to serve as a significant tailwind, reducing the cost of dollar-denominated debt and incentivizing capital inflows into these regions

2. Positive Earnings Growth Expected to Fuel Market Momentum in 2026

-

While room for further multiple expansion may be limited, the good news is that equity markets appear to be transitioning into an earnings-led phase where profits are doing more of the heavy lifting and carrying the performance baton

-

S&P 500 profits are poised for 13% growth in 2026, a path that should underpin equity fundamentals

-

While the U.S. economy may be in the 2%-3% growth range – earnings will likely be much higher

-

We will closely monitor the breadth of corporate earnings growth in 2026. A positive development would be less reliance on the Magnificent 7 and a notable pick up in earnings momentum by the remaining 493 companies

3. Monetary Policy / U.S. Federal Reserve Tilts to Further Easing in 2026, while other Global Central Banks Hit the Pause Button

-

Major central banks collectively cut interest rates throughout 2025, marking one of the fastest-paced easing cycles in many years in response to easing inflation and trade uncertainty. Japan was a notable outlier with rates moving higher

-

We anticipate a pause and hold by most central banks in 2026

-

However, the U.S. should be the exception. The U.S. Federal Reserve will likely be influenced to cut rates given weaker labour market trends, rather than the effects of lingering inflation

-

Growing uncertainty around long-term rates presents a risk. Our preference is to own short-term fixed income securities and utilize other income-oriented investments such as private and alternative investments

4. AI Expansion and Adoption

-

The Trump Administration is aggressively advancing U.S. technology supremacy and its global export. The government has imposed 25–30% tariffs on Chinese tech imports (e.g., semiconductors, telecom equipment) to penalize IP theft and forced technology transfers

-

The AI Action Plan prioritizes streamlining infrastructure, easing regulations, and delivering end-to-end AI solutions to allied nations

-

Pressured allies to adopt U.S.-centric supply chains (e.g., Taiwan Semiconductor’s Arizona chip plant)

-

This AI mega-theme cascades benefits across layers – from semiconductor leaders and hyperscalers to cloud platforms, AI-enhanced enterprise software, cybersecurity, power generation, data centers, etc.

-

Broader industry adoption of AI remains a long-term initiative

Potential Risks

-

Geopolitical Uncertainty – military attacks, trade war with China, etc. could lead to more market volatility, a weaker U.S. Dollar, and rising precious metal prices. Given the current climate of global instability and sustained accumulation by central banks, allocating capital to gold or other precious metals may serve as a vital strategic hedge within the portfolio

-

High Government Debt – limits fiscal policy flexibility, increases scrutiny by bond investors, and leads to sharply higher longer bond yields

-

Persistent Inflation – the impact of tariffs remains a concern on inflation expectations, complicating monetary policy for the U.S Federal Reserve

-

Labour Market Weakness – increasing signs of strain, higher unemployment, limited employment opportunities for the younger demographic, all could lead to higher consumer credit delinquency rates and defaults

Conclusion

In navigating an evolving investment landscape defined by both opportunity and risk, we remain focused on proactive monitoring and disciplined strategic reassessment to stay ahead of shifting market dynamics. We maintain a constructive outlook on equities and other risk assets, and continue to emphasize the importance of constructing resilient, well-diversified portfolios across multiple asset classes. Our approach is supported by rigorous oversight and close collaboration with experienced and specialized external managers and investment strategists.

We also believe private investments, including private credit, private equity, and infrastructure, play a strategic role in portfolio construction by improving diversification, enhancing returns, mitigating inflation and market-related volatility, and addressing specific investor objectives. As conditions evolve, we will implement tactical adjustments where appropriate, always prioritizing long-term performance and alignment with our clients' financial goals.