Andy's Angle

Happy Friday,

The kids are back in school and no better time than to do a quick review of RESPs and how to potentially increase your child’s education fund by 42.5%.

This was a busy week with the release of Apple iPhone 8, which celebrates the 10 year anniversary of the iPhone - a device that changed human interaction and behavior around the world.

number 8 may be a lucky number for the Chinese, but I’m not sure if luck will be enough for this stock. History doesn’t always repeat, but sometimes it rhymes……..let’s circle back in a couple quarters.

Equifax, the world’s leading supplier of consumer and commercial credit information, announced a data breach of 143 million consumers. This is almost half the US population and caused the stock to drop -30% in the last week….

If you are stuck in the city this weekend enjoy the Roncesvalles Polish Festival on Saturday and the Toronto Garlic Festival on Sunday.

Finally, this Angle’s Hot Stocks weighs in on the Clash of the Titans: Dollarama vs. Amazon as well as a dividend play through and Emera Incorporated.

Have a great weekend and happy reading!

Andy’s Angle: Increase your child’s RESP by 42.5%

Registered Education Savings Plan (RESP) 101: Father and Son – Cat Stevens

As many of you know, the RESP is a tax sheltered investment account designed to help families pay for university and college education costs. RESP savings can be used to purchase a variety of ‘education-related costs’ such as books, tuition, rent, food and even a car to shuttle your kid to class.

Every year you can contribute $2,500 into an RESP account and qualify for a maximum government grant of $500. Your child’s 17th birthday is the final year to qualify for the free government grant and with a modest annual return of 5% (the average return of the S&P 500 for the past 30 years is 7.68%) the total amount in the RESP should be $76,575. Pretty sweet, right?

Well, let’s think about it. Current average tuition costs in Canada are $6,373 and rising at 2.8% per year, which could lead to a 4-year university tuition program in 2032 (17 years from now) costing $41,351. Rent of $700 per month today could cost $43,000 in 17 years for four years of university. None of these projections include books, food, utilities etc.. I’m sure you can do the math now…………………Houston we gotta problem

Consider this strategy. The RESP account allows for a maximum one-time contribution of $50,000. If you invest $50,000 upfront, you will not qualify for the free $500 annual education grant ($7,200 total grant) from the government. However, your $50,000 investment should grow to become $109,144 over 17 years at the same 5% annual return. This is +42.5% more than if you had contributed $2,500 per year with the $500 government grant. Even if you invested $10,000 every four years into the RESP, the total amount would grow to become $83,200. The magic of compounding…..it’s beautiful!

Parents should also consider creating joint family RESPs as opposed to individual child RESPs to save on pesky fee costs.

Chart 1: Increase your child’s RESP by 42.5%

Source: RBC Dominion Securities

Andy’s Portfolio Views

Andy’s Portfolio views remain largely unchanged from the previous edition with an overweight to Technology, Financials, US and Continental Europe. One noticeable change is the strength in the healthcare sector which I will be taking a closer look at over the next few weeks.

Andy’s Hot Stocks: Dollarama vs. Amazon – Clash of the Titans, Emera – An income alternative

Dollarama: I need a dollar dollar, a dollar is what I need – Aloe Blacc

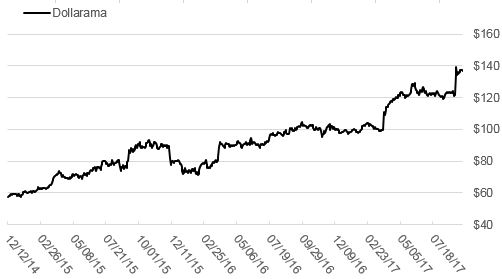

TSE: DOL Price: $134 +42.2% since 12-31-2016

A little bit of CanCon for you. Dollarama is quite possibly the highest quality retail/consumer stock in Canada…...period. Dollarama has a business model that is defensive during recessions (low-priced items) and benefits during boom-periods (increased foot traffic). The company has a simple business model with stores that practically run themselves and consistently capitalize on any holiday. Walk into a store the day after Thanksgiving and you will see Christmas items ready to go.

The highest priced items in Dollarama are still only $4.00 which pales in comparison to its US competitors and also makes it somewhat immune to the Amazon threat. The stock is expensive at a 30x PE ratio, but organic sales are growing at 6.1%, new store square footage is growing at 4-5% and earnings are growing at 30% year over year. Dollarama broke out after its second quarter earnings release and we recommend investors wait for the stock to consolidate for a couple months before purchasing. Put it on your watch list for the time being.

Chart 2: Dollarama’s still get some levers to pull

Source: RBC Dominion Securities, Thomson Reuters

Amazon: Crushing entrepreneurs dreams since 1994 – The Last Mall – Steely Dan

NYSE: AMZN Price: $977 +28.1% since 12-31-2016

This stock has been front and center of financial news for the past three years. Jeff Bezos has gone toe-to-toe with Warren Buffet as the richest man in the world for the last couple months. I’m not going weigh in on the winner.

Let’s talk a bit about Amazon’s business. The online retail business is barely profitable with operating margins at 1.9% (worse than a grocery store). Their push for market share has decimated the US retail sector with companies like Macy’s and Nordstrom getting crushed. The US and Canadian grocery market are likely next on the chopping block.

Amazon Web Services has been the key driver of the stock. This is the cloud computing business that is growing sales at 42% and has operating margins of 22%. This business unit is only 10 years old and is the largest cloud service vendor in the world. Boom.

If you work in retail, hedge your bets and buy some Amazon. If you don’t work in retail, buy it anyways.

Chart 3: AMZN is decimating retailers with 500% outperformance vs. traditional retailers

*Graph has been rebased to 100

Source: RBC Wealth Management, Thomson Reuters

Emera: The quest for yield continues – Barrett’s Privateers- Stan Rogers

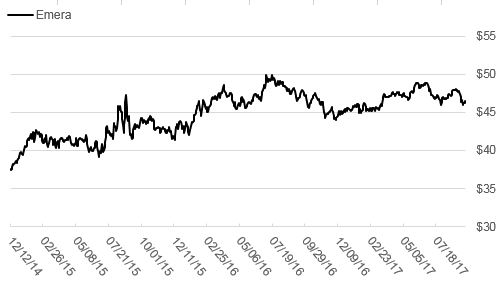

TSE: EMA Price: $47 +8.6% since 12-31-2016

Interest rates remain at historical lows despite the recent increases by the Bank of Canada. As a result, investors that rely on income and stability have suffered with bond yields at record lows and our highest 2 year GICs returning a measly 2.08%. This is only marginally above the latest inflation print of 1.2% and below Canada’s long-term inflation rate of 3.15%. I remain underweight the utility sector, however consider this income alternative.

Emera is a diversified utility company based out of Canada’s Ocean Playground, Halifax, Nova Scotia, and has businesses throughout North America. The company’s emphasis on energy distribution vs. generation results in a more stable business model. Furthermore, Emera’s focus on clean energy generation could become an advantage as clean energy becomes more of a standard for power generation and distribution.

Emera is a high-quality company with industry-leading cash flow return on capital and consistent dividend growth. The stock currently has a 4.4% dividend yield and investors can benefit for the Canadian dividend tax credit. Emera stock is 34% less volatile than the market and provides a service that will always be needed……electricity.

Chart 4: Emera- Steady as she goes

Source: RBC Wealth Management, Thomson Reuters