Volatility was relatively subdued over the past week, helping global equity markets edge higher. The COVID situation remains a near-term headwind but not enough to dissuade investors from the view that a sustainable growth trajectory is around the corner. Meanwhile, the first quarter earnings season is now underway with companies reporting results amidst relatively high expectations. We explain some early takeaways from the banks, and discuss what we’ll be watching as the next few weeks unfold.

Coronavirus Update

Discouragingly, the past week saw yet another acceleration in the rate of growth of new COVID cases across Canada. The country’s 7-day average rate of new daily infections rose to over 8,500, from 6,400 the week before, representing a new record high. Manitoba led the way, after having enjoyed a few months of relative stability, and the increase has sparked a new round of restrictive measures in the province. Ontario also saw a sharp increase despite the fact it had already recorded rapid growth in infections for well over a month. Quebec, Alberta, BC, and Saskatchewan also saw notable increases though not as severe. The situation in Atlantic Canada and the northern territories remains relatively stable.

The story is similarly frustrating in many other jurisdictions. India reported a record of more than 210,000 new daily cases, surpassing the 130,000 record reported in the prior week. Chile, Japan, Germany, and Turkey are just a few of the other countries facing an accelerating spread at this point. The U.S. has witnessed a rise in its daily trends over recent weeks, but not at the pace of others.

Israel represents the best example of what hopefully lies ahead for most countries. After having witnessed a record high of more than 10,000 new daily cases in late January, it has seen its figures fall below 200 recently, driven by an aggressive and efficient vaccination campaign that has seen more than half of its population of 9 million people receive their jabs.

Strong Growth Expected

The first quarter earnings season, measuring business results between the months of January to March, has officially kicked off. Expectations are high, with consensus calling for 25% year-over-year growth for companies within the S&P 500 index, the most popular benchmark for the U.S. equity market. Moreover, the earnings growth rate for the second quarter (April to June) is expected to rise by more than 50%, reflecting the fact that much of the world’s economy was shuttered in the spring of 2020. For the full year, the average estimate is for nearly 26% year over year growth. This stands in stark contrast to the decline of almost 13% that was witnessed last year.

Many U.S. banks reported results over the past week. Unsurprisingly, many are releasing some of their credit provisions, after having built them up significantly nearly a year ago in preparation for loan losses. Meanwhile, revenues across capital markets businesses and wealth management franchises were strong, driven by a positive market backdrop. One source of potential disappointment may have been net interest margins, which measure the difference between interest paid to depositors, and interest earned from borrowers. Investors expect this important source of profitability to improve this year along with the rise in bond yields witnessed year-to-date. But, management teams highlighted that any improvement will take time. U.S. consumers are not yet ready to re-lever, as many have accumulated savings from the significant government stimulus deployed over the past year. These reserves may need to be spent before demand for loans re-emerges and drives an uptick in margins. Overall, the results were in-line with high expectations and served as confirmation that the economic backdrop, at least in the U.S., is improving.

Management teams from a range of sectors will be commenting on their own company results over the next few weeks. We look forward to any insight they can provide with respect to the outlook on costs and inflation. Everything from lumber, to coffee, skilled labour for certain industries, and semiconductor “chips” are all seemingly in short supply. Any sustained supply issues could present cost and profit margin headwinds to companies across a number of industries. It may be premature to be overly concerned at this juncture, but it is something worth monitoring.

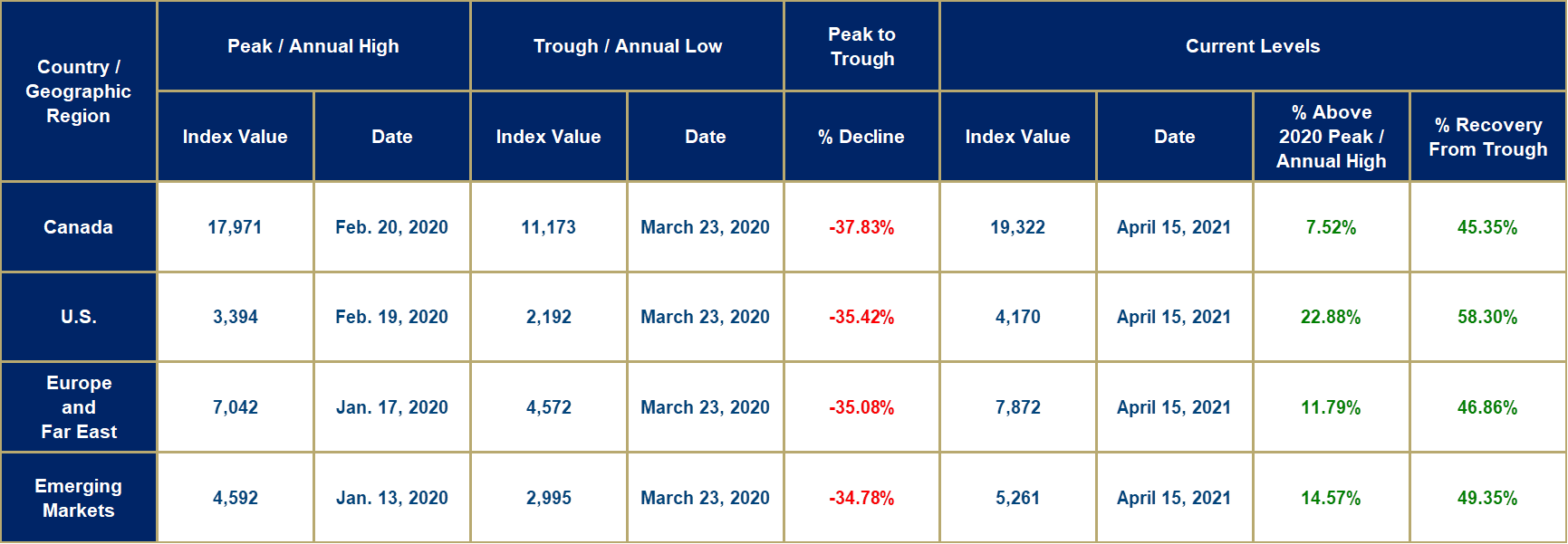

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of yesterday’s (Thursday, April 15th) closing prices.