It was an interesting week to say the least. Volatility surged for a brief period and then meaningfully retreated. Instead of the usual fundamental developments – the economic trajectory, path of the virus, interest rates, government policy, and earnings – it was a series of extreme swings in the prices of a handful of smaller and heavily “shorted” stocks that caught the markets by surprise. It’s an evolving story that makes for good headlines but has little to do with the broad outlook for the economy and markets going forward. We explain below. We also provide an update on the COVID front, and discuss the inflation conundrum that is likely to surface at some point in the year ahead.

An Online-Driven Short Squeeze

A number of obscure and smaller stocks around the world witnessed extreme price moves over the past few weeks. One common characteristic has been that each of these stocks had been heavily “shorted” prior to the recent action. A “short” is a position some investors – typically institutional in nature – take when they believe that the price of a stock will fall.

Over the past week, it was revealed that a large online community of retail investors have been responsible for the surge higher in these stocks. Acting together, they were able to buy vast amounts of shares and options in these stocks, bidding up the prices and forcing some of the institutions to unwind their “short” positions, which then exacerbated the upside pressure creating a sort of feedback loop.

This development caught many by surprise given the extent of some of the moves. The fact it was fueled by some degree of coordination among retail investors socializing online was also noteworthy. While it has limited implications for the outlook for the economy and markets, it highlights the growing force of a retail investor base that is willing to increasingly collaborate. However, we can’t help but wonder how many of these investors are motivated by the potential for gains they perceive to be quick, extreme, and easy. Some have likely undertaken the proper due diligence, but many may be paying little attention to the business value underlying some of these equities. Ultimately, we expect fundamentals will return at some point, as they always do, to be the biggest driver of these share prices.

Coronavirus Update

On the COVID-19 front, the peak of the second wave of the virus in Canada – and third in the U.S. – appears to be behind us. Canada’s 7-day average rate of new daily infections fell again this past week, at just over 5000 versus the 6000 from a week ago. Once again, all provinces saw declines, with Ontario, Quebec, and Alberta leading the way. New Brunswick, which had seen a spike in recent weeks, saw a fall in its average. Meanwhile, the northern territory of Nunavut has seen no new cases in recent days, which is reassuring given a significant one day jump in new infections nearly a week ago. The U.S. also saw another week of notable progress. Its 7-day average rate of new daily infections fell below 150,000, versus the nearly 180,000 from a week ago.

A number of regions around the world – Malaysia, Peru, Brazil for example - haven’t seen the same kind of progress witnessed in North America of late. But, there may be more help on the way. U.S. biotechnology company Novavax released data from two clinical trials in recent days. Its vaccine candidate demonstrated an efficacy rate of 89% in the U.K., and showed it protected against the U.K. variant of the virus. Meanwhile, in South Africa, where another variant is prevalent, Phase 2 trial results demonstrated an efficacy rate of 60% in people without HIV. Moreover, Johnson & Johnson is expected to reveal results of its trials in the coming weeks. We see high odds of more vaccines being approved in the months to come.

The Inflation Conundrum to Come

One issue that bears monitoring as we transition through the year is the likelihood of upward pressure on the prices of goods and services.

Inflation is most commonly measured by the year over year change in prices for goods and services. In 2020, the rate of inflation, particularly for services, fell precipitously at the onset of the pandemic. In the year ahead, we see potential for the economy to move from partially open to nearly fully open. That transition should translate into a meaningful acceleration in growth and consumption. Moreover, despite unemployment that remains elevated, there is a substantial amount of savings that consumers have accumulated following the actions taken by governments. All of this could stimulate an environment characterized by higher prices for goods and services this year.

A jump in inflation is normally a cause for concern. First, it leads to higher input costs for companies, presenting an overhang to margins and earnings growth. In addition, central banks typically raise interest rates in an effort to curb price pressures. This has a tendency of acting as a headwind to growth. Moreover, the valuations of most assets – stocks and bonds – are heavily dependent on interest rates. Generally speaking, higher rates can lead to lower valuations.

But, the circumstances currently remain far from normal. As a result, the increase in inflation this year may prove to be temporary. That was the view expressed by the U.S. Federal Reserve this past week. They believe the output gap, high unemployment, and longer-term pressures such as technological advancements among other things will impede inflation from permanently rising. They also reminded investors that they are prepared to have inflation run higher than their long-term target for some time before considering any change in its interest rate policy. This shift in their approach was announced last year as they admitted that inflation has more often than not fallen short of their long-term target.

We tend to agree with the approach and comments from the U.S. central bank. The global economy remains relatively fragile, and it is sensible to ensure the economy is on a sustainable path higher before becoming too preoccupied with rising inflation. Nevertheless, we wouldn’t be surprised to see the bond and equity markets wobble at some point this year as they adjust to a more inflationary environment where investors are likely to debate whether the pressures are transitory or more durable in nature.

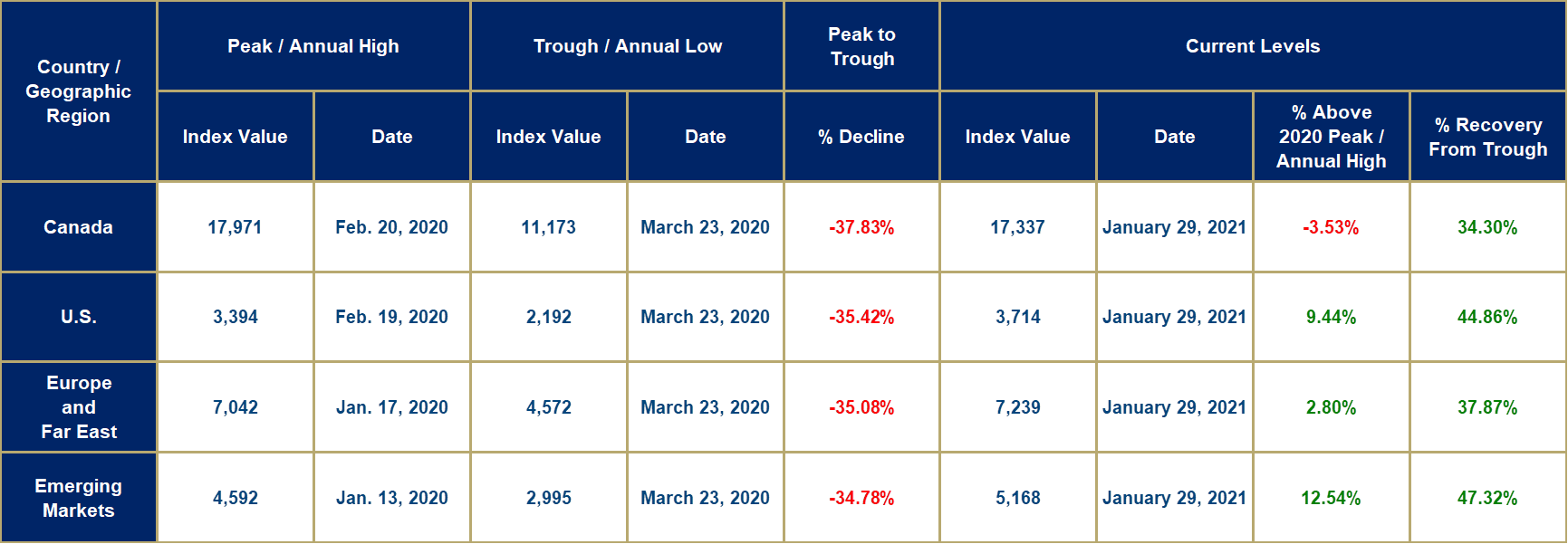

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices.