Global equity markets have been calm and remain near their highs for the year as we close in on the holiday season and the end of a tumultuous 2020. As we share our final thoughts this year, we provide an update on the coronavirus, which continues to present a challenge across wide swaths of the world. We discuss the outlook for 2021 and conclude with reflections and learnings from the year that was.

Coronavirus

The second wave of the coronavirus is proving to be much more difficult to contain than the first. There may be a myriad of reasons – the cooler seasons in the northern hemisphere, a potentially more infectious virus, and overall “virus fatigue” that has led to people letting their guards down. At current levels, nearly 650,000 new people around the world are getting infected every day.

Canada has seen progress over the past week with a meaningful moderation in the rate of new infection growth. In fact, the new infection rate hardly changed, with the country’s 7-day moving average of new daily infections sitting near 6,650, versus the 6500 from the prior week. Some provinces saw meaningful declines in new infection growth: Saskatchewan, Alberta, and Manitoba. Meanwhile, the East Coast and British Columbia were relatively stable. Ontario and Quebec unfortunately have experienced a pickup in the growth rate of new infections. As a result, both provinces are exploring additional restrictive measures in light of the rising pressures facing the health care systems.

After a few weeks of apparent progress, Europe experienced a setback over the past week. Germany’s situation has deteriorated and it has entered a more restrictive lockdown. The Netherlands has followed a similar path. Meanwhile, France and the United Kingdom, which had been improving, saw a pick-up in new infections recently, leading the latter to adopt more restrictive measures in some parts of the country. With some countries temporarily easing their measures over the upcoming Christmas holiday, the infection trends may worsen over the near-term. Meanwhile, the U.S. is averaging over 200,000 new daily infections. The country’s spread remains broad-based, but the state of California has emerged as a hot spot with well over 30,000 new infections every day. Large portions of the state are under lockdown but it has yet to have had an impact on infection trends.

Elsewhere, countries across the world ranging from Russia, to Japan, South Korea, South Africa, and Brazil are all facing rising trends of new infection growth, illustrating the global nature of this crisis.

Thoughts for 2021

We expect 2021 to be a tale of two halves. In the early going, the virus will continue to remain a headwind to economic and earnings growth, as it has for much of this past year. As vaccines become more widely available in the developed world into the spring and summer months, we expect a gradual return to more normal levels of activity, setting the stage for a more durable economic trajectory by the end of the year. Low interest rates and aid from governments around the world, including an additional round from the U.S., should help bridge the economic gap that will exist through this period.

Interestingly, the hit to the global economy from this second wave has not been as negative as expected despite the renewed restrictions across Europe, Canada, and parts of the United States. Recent data from Europe indicates activity – both manufacturing and services – has been more resilient despite recent headwinds. Commentary from both the Bank of Canada and the Federal Reserve officials of late has suggested the respective economies have been a bit stronger than anticipated, although they acknowledged the elevated risk and disparity that exists among different parts of the economy.

In sum, the backdrop of a very low interest rate environment, significant government aid that may extend further, and a more durable economic recovery should help drive meaningful earnings growth. The challenge for investors is that markets are forward looking in nature, and already reflect much of the projected path that we foresee. As a result, while we are constructive on global stocks given improving trends, our level of enthusiasm is relatively modest.

Reflections on 2020

This was an unusual year in so many ways, with concerns spanning personal health, safety, job and business security, and financial risk. Yet, lessons from past crises served to be useful with respect to the management of our client investment portfolios. More specifically, having a properly constructed financial plan that ensures our portfolios are constructed and managed to meet the needs of our clients. In addition, maintaining a level of discipline to control one’s emotions and look past the short-term. Lastly, being prepared to be proactive through rebalancing and identifying opportunities that arise when markets reach extreme levels of pessimism and optimism.

On a final note, we want to wish you and your family a healthy and safe holiday season. We also wish all the best to the health care and front line workers who will remain in the thick of things as they work through this holiday season in less than ideal conditions. We look forward to a new year that we expect to bring an eventual and much welcome return back to normal.

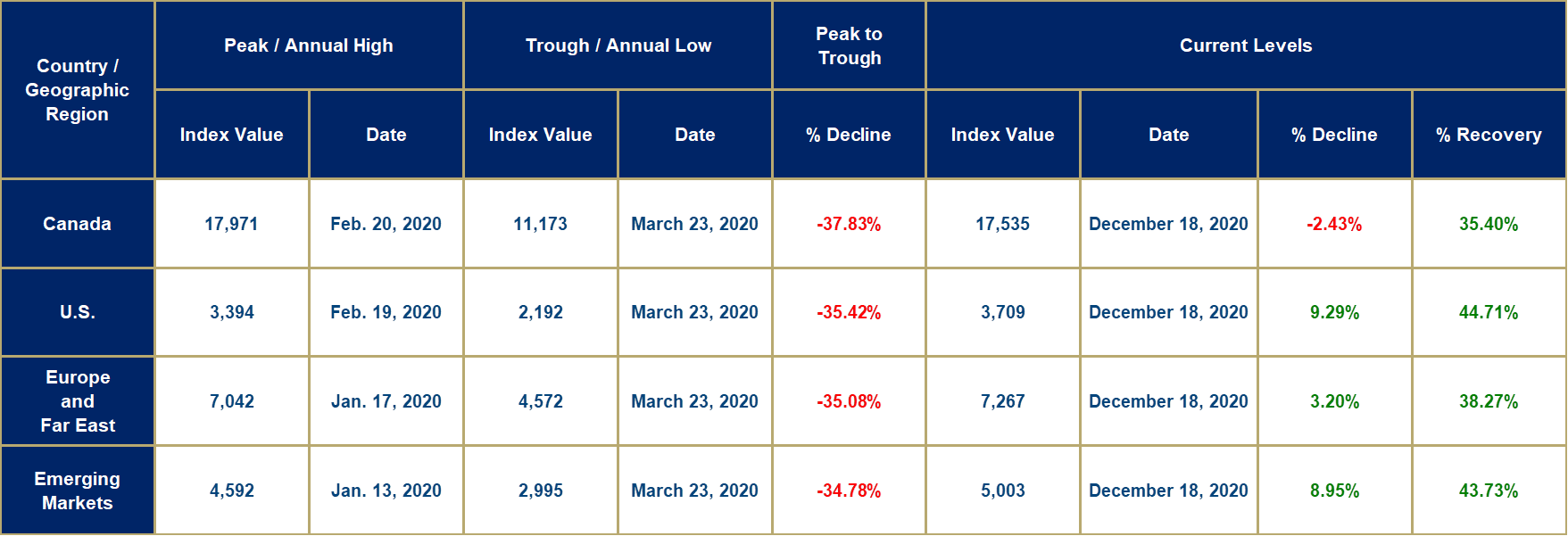

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices.