It was a week full of drama. Yet, the biggest surprise was not the U.S. elections. Rather, the unexpected collapse in volatility in the days that followed, which spurred a sharp global equity market rally. This happened despite the uncertainty that still lies in front of us. We explain more below, including our thoughts on some implications for equity markets going forward. We finish with a brief update on COVID-19, which remains a significant challenge.

U.S. Elections

The market action over the past week was surprising to many. Yet, it is worth remembering the lead up to the U.S. elections involved some pain for investors. Prior to this week, volatility had jumped and global equities sold off based on a variety of concerns: a second wave of COVID-19 that has been spreading faster than expected, and the elections. On the latter, the worry was twofold: the risk of a contested outcome and investor anxiety over a “blue wave” scenario in which the Democratic Party would control the presidency and both chambers of Congress. This potential outcome presented the risk of more sweeping policy shifts such as the removal of tax cuts implemented a few years ago and a heightened regulatory environment. The results to date suggest the odds of a “blue wave” have fallen meaningfully, helping to reassure investors despite some uncertainty around the elections that remain.

We appreciate the degree of election fatigue that now exists. However, it is worth briefly reflecting on where the results stand. As a reminder, there were three elections: the presidency, the House of Representatives, and the Senate.

With respect to the presidential elections, Democratic candidate Joe Biden has 253 electoral votes to President Donald Trump’s 213. To win the White House, 270 electoral votes are needed. There are five states that have yet to confirm a winner: Arizona, Georgia, Nevada, North Carolina, and Pennsylvania. Joe Biden needs to win one or two states, while Donald Trump needs to win at least four. The race in each of these five states remains incredibly close.

On the congressional side, the Democratic Party has fallen short of expectations. They appear set to keep their majority in the House of Representatives despite losing a few seats. Meanwhile, in the Senate, the path for them to win a majority has narrowed significantly as they were unable to win states that were considered toss-ups. There is still a slim chance with a “runoff” election in January in the state of Georgia. The Republican Party’s success in the Senate race has helped reduce the odds of a “blue wave” scenario.

We expect more clarity on the presidential election in the coming days, perhaps as early as today, as all five states complete the counting of ballots. But, even then, some doubt may linger, and there is a high likelihood of recounts. Several legal challenges have already been submitted in many of the battleground states, including Georgia, Michigan, Wisconsin, and Pennsylvania. We are not litigation experts, and so it is difficult to offer much of an assessment. Nevertheless, we expect this to drag on longer than we would have preferred.

Implications Going Forward

It may seem premature to discuss implications of an election that has yet to conclude, but there is more clarity today than a week ago given the likelihood of a divided Congress. First, the probability of a large and far-reaching round of fiscal stimulus appears to now be off the table. Instead, a smaller package is more likely as both parties will have to come to an agreement. Meanwhile, any plans to increase taxes on corporations and individuals will be more limited in nature. Lastly, we expect less risk of disruption from any new regulations. Industries such as technology, health care, financial, and energy may be less encumbered than they otherwise would have been under a “blue wave” government.

Coronavirus

Unfortunately, the trend of rising COVID-19 infections around the world continued this week. Globally, we have reached 500,000 new cases and 6,500 new deaths daily.

Despite the actions undertaken by several European countries, the upward trend in infections has yet to significantly change. Meanwhile, fatalities linked to the virus have continued to climb. Although some of the broader nationwide lockdowns have only been in place for close to a week, governments are hopeful the actions taken will eventually curb these trends. Time will tell but it has been a formula that has proven successful in the past. In the U.S., the country reported a record of more than 100,000 new daily infections this week. Hospitals across southern and Midwestern states such as Oklahoma, Missouri, North Dakota, and Idaho are showing signs of strain, suggesting more restrictive measures may be needed.

In Canada, the 7-day moving average of new daily cases is over 3,200 versus the 2,750 from the previous week. Outside of the northern territories and the East Coast, all provinces saw an increase. Alberta did see a slowing in its rate of new case growth, while Quebec and Ontario’s changes were relatively modest. Elsewhere, Manitoba continues to lead with the fastest increase in its new daily infection rate, while Saskatchewan and British Columbia also saw alarming increases relative to other provinces.

In closing, we circle back to the issue of uncertainty. Despite the drama that unfolded over the past week, investors now have some more clarity with respect to the Congressional make-up of the next U.S. government. And, as mentioned, we expect less extensive action with respect to taxes and regulation. This should help provide a supportive backdrop for consumers and businesses. We expect investors to gradually turn their attention back to the economy and the earnings recovery that remain key to the outlook for markets in the year ahead.

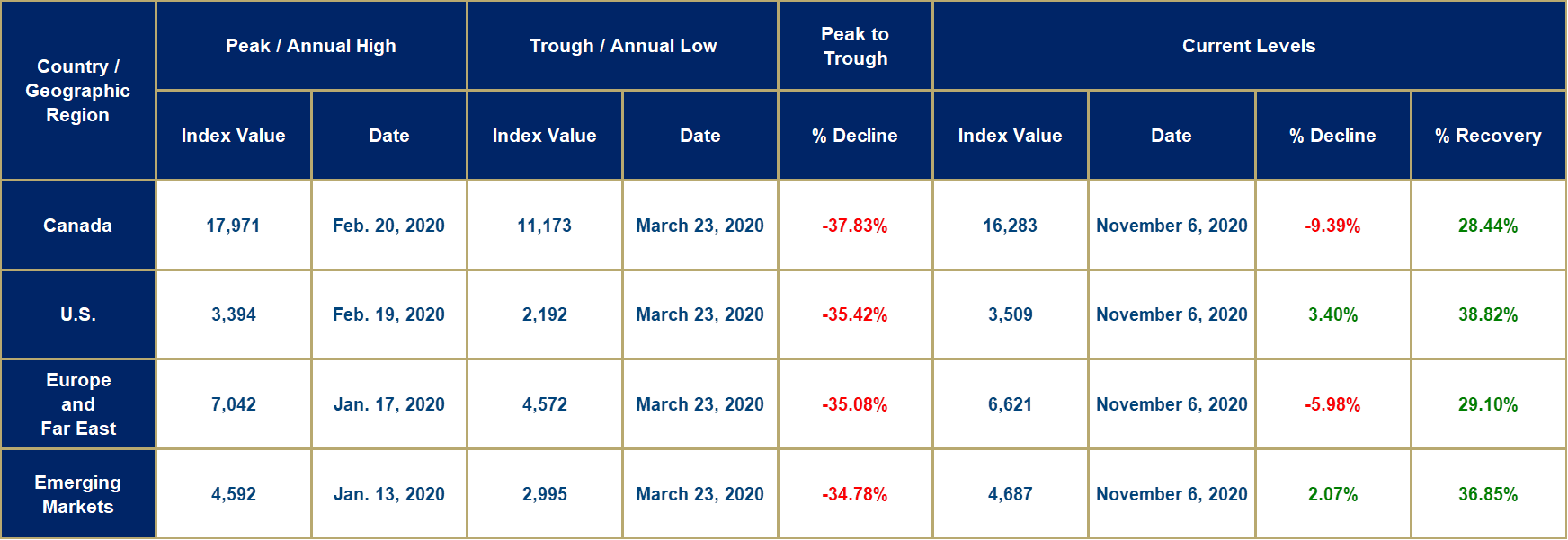

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices.