Markets were relatively unchanged over the past week with investors coming to terms with the low likelihood of an imminent U.S. stimulus package as well being focused on the spread of the coronavirus. This week also marked the official start to the earnings season. We discuss the notion that while the outlook for businesses remains murky and company results may not look good on the surface, the trend itself is improving.

Coronavirus Update

Europe was largely in focus over the past week given deteriorating conditions across the region as a whole. France, Poland, the Netherlands, Italy and Germany are among some of the countries that have reported record highs in new daily cases over the past week. Meanwhile, Spain continues to see elevated figures and has expanded the number of cities facing lockdown. The United Kingdom is expanding its restrictions by employing a tiered approach to regions across the country. The services sector of the European economy had already showed signs of moderating since late summer and that trend looks set to continue in the wake of the restrictive policies being put in place.

The virus continued its spread across Canada over the past week. But, there were some notable differences versus recent weeks. First, an overall moderation in the rate of growth of new cases across the country. The 7 day moving average now stands at over 2300 new cases per day, just 300 higher than the level from a week ago. The province of Quebec continues to have the highest volume of new daily cases, but its rate of growth has declined. Meanwhile, Ontario and British Columbia’s average new daily case figures rose again but the rate of change paled in comparison to Saskatchewan, Manitoba, and Alberta, all of whom saw a meaningful acceleration in the rate of new daily infections. Even the Maritimes saw its first notable uptick, largely in New Brunswick. Fortunately, the case numbers on the East coast remain low in absolute terms.

Lastly, the United States is experiencing a steady rise of new infections as well. In contrast to the spring and summer, this spread can be characterized as being more broad-based with well more than twenty states experiencing rising new daily cases. Interestingly, some less populated areas are facing high concentration of infections per capita. These include: North and South Dakota, Montana, Wisconsin, Nebraska, and Utah to name a few.

Earnings Season Is Upon Us

The third quarter earnings season is now upon us, with hundreds of companies across Canada, the U.S., and Europe expected to announce results over the next month. The period encompasses the months of July through September.

The expectation for the U.S. market, where data is more readily available and widely followed, is for this quarter’s earnings to fall by nearly 20% year over year. In absolute terms, that is quite weak. Moreover, of the companies that historically provide annual guidance, more than half of them continue to withhold guidance for this year and next, due to the lack of clarity on the business outlook.

Yet, things are improving. The decline in earnings expected this quarter is less than the 30% decline seen last quarter. Furthermore, there has been a steady increase in the number of companies now willing to provide an outlook. And for the most part, the guidance has been better than expected with the number of companies issuing positive “pre-announcements” outpacing the number of companies warning of weaker than expected results.

This shouldn’t be too surprising. The economic data has itself improved through the summer and into the fall and has likely helped the operating environment for some businesses. To be clear, it remains far from normal, and we still expect it to take a year, if not longer, for the global economy to attain the levels we saw in 2019. But, we are comforted by the progress that continues, even if it may moderate to some extent as a result of the increasing restrictions that governments are embracing in various parts of the world to stem the spread of the virus and ease the burden on their health care systems.

We are eager to hear from various management teams in the weeks to come when they release their results. Their commentary may help provide some clarity on whether they are growing more comfortable in the sustainability and resiliency of the economy and business climate. We look forward to sharing some of our key takeaways in the not too distant future.

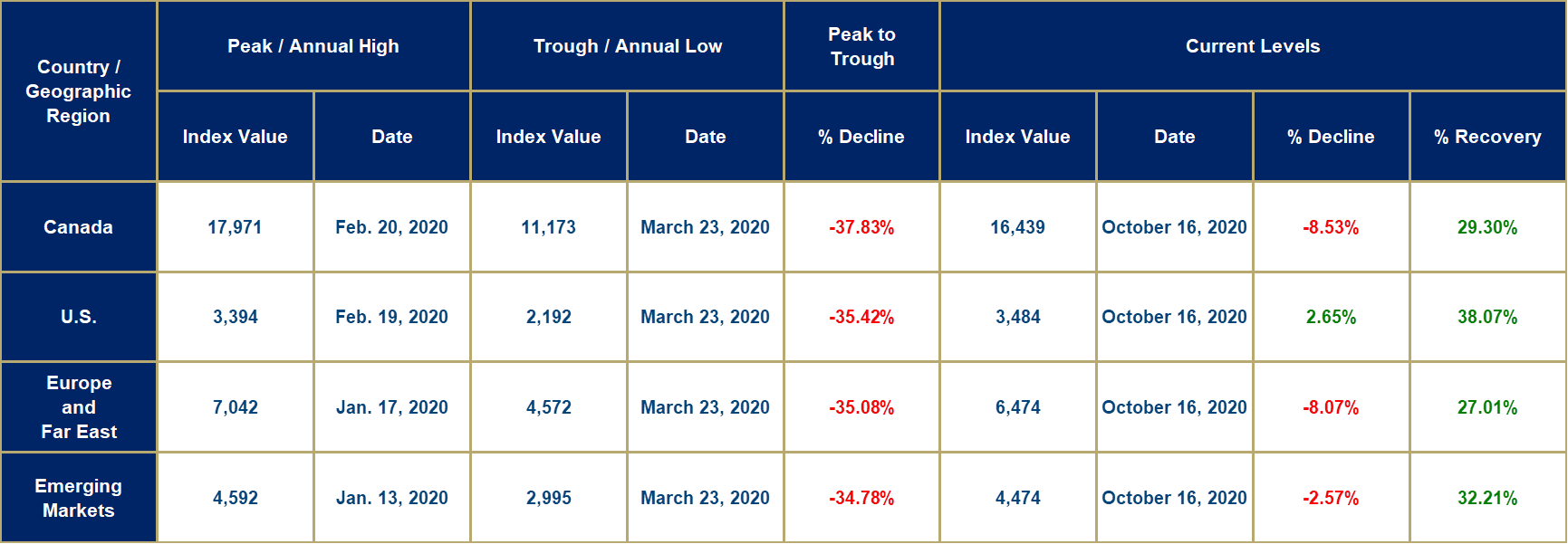

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today's closing prices.