Global equity markets experienced some weakness this week, though the decline was sparked by no obvious catalyst. The week was also highlighted by a combination of hope on the vaccine front and global economic data for the month of August that suggest the recovery is continuing, albeit at a pace that has moderated. We share our thoughts below.

Market Selloff

The selloff that occurred was notable because it was accompanied by a meaningful jump in volatility, though levels remain well below the extremes seen earlier this year. Furthermore, the selloff was led in particular by the so-called “growth” stocks that have been responsible for leading the global markets higher in recent months. But the ingredients for this week’s decline may have started to come together weeks ago as there was growing evidence that fewer stocks were making new highs despite the market itself moving higher. This is often regarded as a lack of “breadth”, which can sometimes foreshadow future weakness. These market conditions can be described as normal given the fact that we have experienced several weeks over the past few months in which markets have improved, so it's not surprising that we are seeing some weakness.

Coronavirus Update

COVID-19 trends remained largely the same over the past week. More specifically, the number of new cases in the U.S. continues to grind lower. Other jurisdictions are also seeing progress in the form of relatively stable numbers, namely Australia, the African continent, and Russia. Elsewhere, some countries are grappling with high or accelerating new cases, including India, Spain, and France. From the market’s perspective, these trends are not surprising, and it may view the lower fatality rates in recent months and measured approaches governments have taken as a sign that economies can function and even recover while the virus is out there. Furthermore, hope remains on the vaccine front. This week, it was revealed that the U.S. Center for Disease Control and Prevention reached out to all states to ensure they are ready to distribute a vaccine as early as November, should one be ready. It remains unclear as to if and when a vaccine will be approved, but the gesture alone understandably ignited a dose of optimism.

Economic Recovery Continues Despite Slowing Momentum

On the economic front, there was much to digest this week. The global services sector, which includes businesses in areas such as hospitality and leisure for example, was hit particularly hard this year given the nature of the health crisis. But, data for the month of August across Europe, Asia, and North America suggested that this part of the global economy is continuing to recover; albeit at a moderated pace. This slowing may be a function of a normal leveling off following a strong initial rebound in recent months, or it could be a result of something more worrying such as renewed concern on the part of consumers or localized lockdowns in certain areas that have faced a resurgence of the virus.

Separately, employment figures across North America suggest a similar trend of ongoing recovery but moderating momentum. Canada and the U.S. both saw another month of employment gains in August. Inevitably, some investors will focus on the fact that nearly half of the jobs lost across North America during the peak of the pandemic have now been recouped (to be precise, more than half of the jobs lost have been regained in Canada). Others are likely to emphasize the fact that millions of people still remain unemployed and are depending heavily on government programs. We think it’s important to recognize that meaningful challenges remain, but to also understand that we are in a period of healing and recovery that will take time.

This week marked the beginning of September. As a result, we are turning our focus to the fall season and the issues that could have important consequences for the economic and investment outlook. These include the return to school, which promises to be unlike any other. Meanwhile, the widely used Canadian Emergency Response Benefit (CERB) transitions to new and more permanent programs at the end of this month. A throne speech from Prime Minister Justin Trudeau, also later this month, may prompt a confidence vote and offer an opportunity for opposition parties to respond. Lastly, the U.S. elections take place in less than two months and will undoubtedly garner much investor attention in the weeks to come.

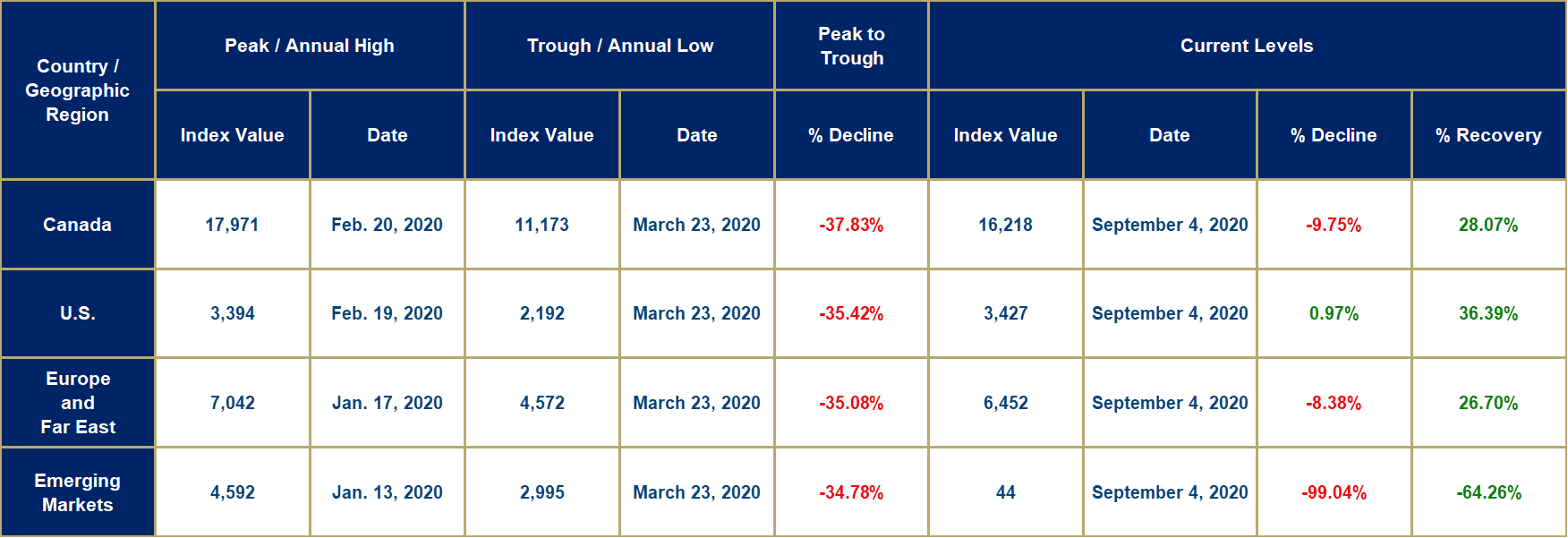

Market Decline and Recovery Results

The peak-to-trough numbers for the current market decline and subsequent recovery are provided in the table below, as of today’s closing prices. All four major market regions have stalled a little recently.