Imagine it is early January 2010 and you are reading a review of the financial markets. Investors have been on a roller coaster over the past three years, living through the stress of the global financial crisis and market downturn of 2008–2009, then experiencing the recovery that began in March 2009 and is still going strong.

Investors who rode out the market’s slide are beginning to be rewarded. But the rebound is 10 months old, and markets have a long way to go to reach their previous highs. Opinions are mixed about what might unfold in the coming year. A December 2009 headline in the Wall Street Journal underscored the uncertainty: “Bull Market Shows Signs of Aging.”1 The publication pointed out that, although stocks have rallied and indices are on the rise, worries are mounting in some quarters that the market is running out of steam.

From the vantage point of early 2010, you may be wondering whether to stick with your investment plan or move into cash and wait for more evidence that the markets have recovered. Now, fast forward to today and consider what the global equity markets delivered to investors who stayed the course.

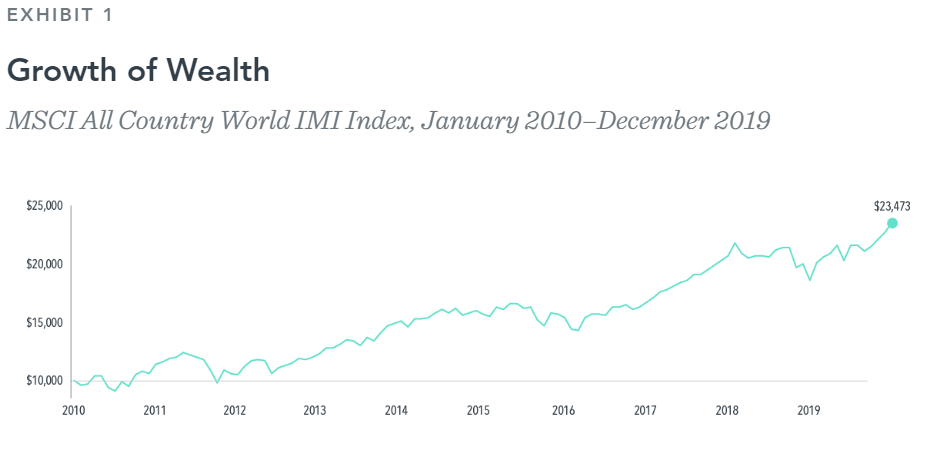

On a total return basis, global stocks more than doubled in value from 2010–2019, as Exhibit 1 shows. The MSCI All Country World IMI Index, which includes large and small cap stocks in developed and emerging markets, had a 10-year annualized return of 8.91%. From a growth-of-wealth standpoint, $10,000 invested in the stocks in the index at the beginning of 2010 would have grown to $23,473 by year‑end 2019.

Source: MSCI. In US dollars, net dividends. MSCI data © MSCI 2020, all rights reserved. Index is not available for direct investment. Performance does not reflect the expenses associated with management of an actual portfolio.

Despite positive annual market returns during most of the decade, investors had to process ever-present uncertainty arising from a host of events, including an unprecedented US credit rating downgrade, sovereign debt problems in Europe, negative interest rates, flattening yield curves, the Brexit vote, the 2016 US presidential election, recessions in Europe and Japan, slowing growth in China, trade wars, and geopolitical turmoil in the Middle East, to name a few.

The decade also brought technological advances in electronic commerce and cloud computing, the global embrace of the smartphone and social media, increased automation and enhanced artificial intelligence, and new products like electric cars and early iterations of self‑driving ones.

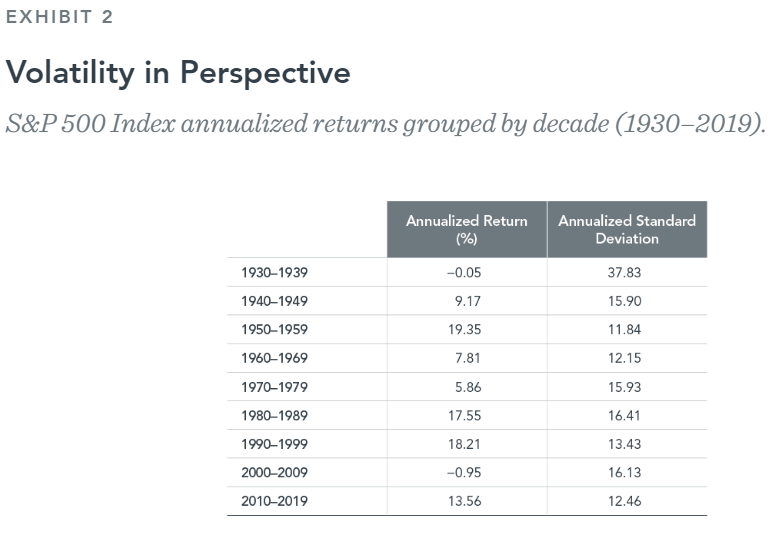

Looking back, you could conclude that the decade had its share of uncertainty—just like the decades before. But overall, the US equity market experienced moderate volatility compared with previous decades. Exhibit 2 displays this by looking at returns and standard deviation, where a higher standard deviation reflects wider market swings during that decade.

In US Dollars. S&P 500 Index data provided by Standard & Poor’s Index Services Group. Standard deviation is a statistical measurement of historical volatility.

Benefits of Diversification

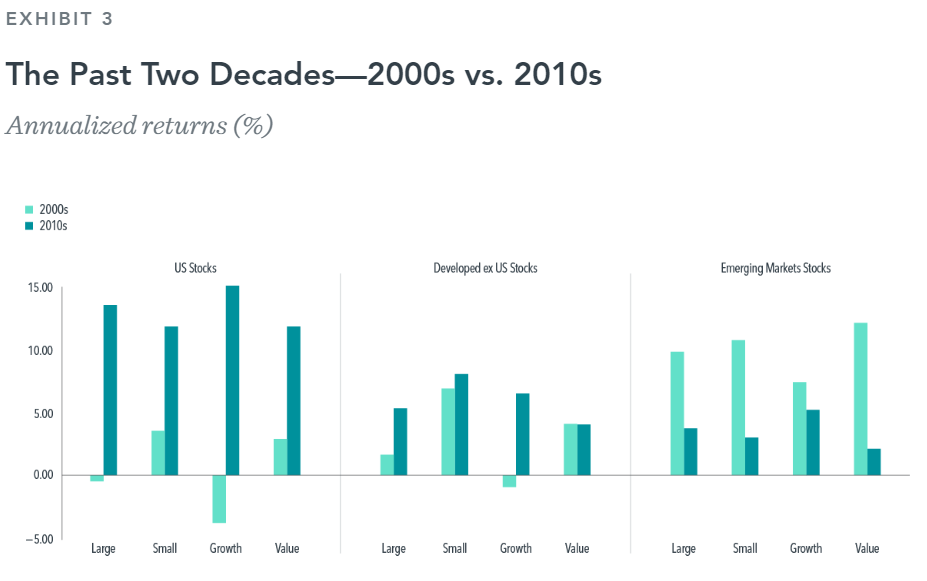

Investors who committed to global diversification and to areas of the market associated with higher returns—small cap stocks and value stocks (i.e., stocks trading at low relative prices)—were challenged over the past decade. As shown in Exhibit 3, during the 2000s, investors were generally rewarded for holding emerging markets stocks and developed ex US stocks. During the 2010s, the US market outperformed developed ex US and emerging markets.

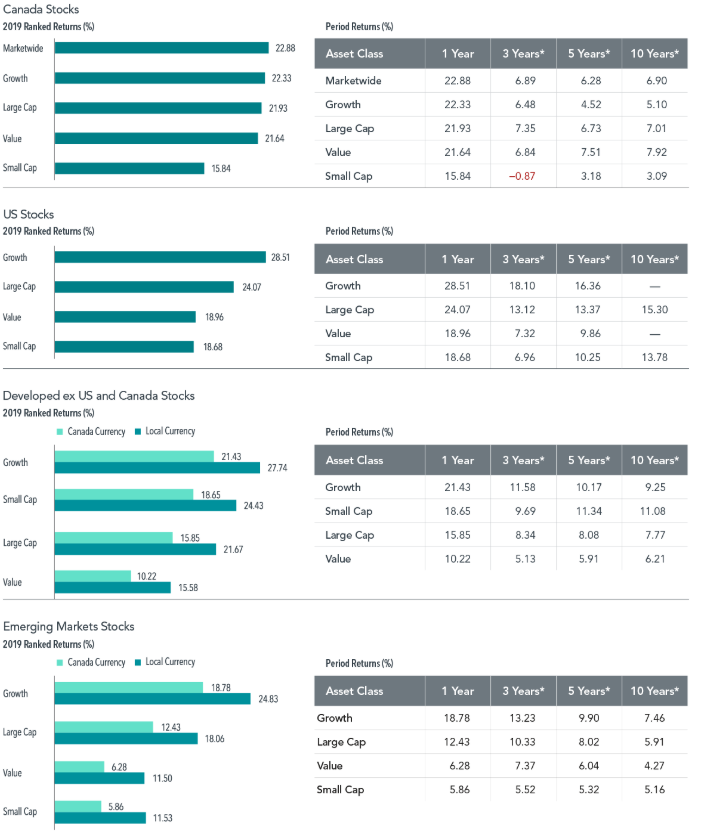

Market segment (index representation) as follows: US Stocks—Large Cap (Russell 1000 Index), Small Cap (Russell 2000 Index), Growth (Russell 3000 Growth Index), Value (Russell 3000 Value Index); Developed ex US Stocks—Large Cap (MSCI World ex USA Index), Small Cap (MSCI World ex USA Small Cap Index), Value (MSCI World ex USA Value Index), Growth (MSCI World ex USA Growth Index); Emerging Markets Stocks—Large Cap (MSCI Emerging Markets Index), Small Cap (MSCI Emerging Markets Small Cap Index), Value (MSCI Emerging Markets Value Index), Growth (MSCI Emerging Markets Growth Index). Index returns are in US dollars, MSCI indices are net of withholding tax on dividends. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2020, all rights reserved. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

The performance of value stocks vs. growth stocks (i.e., stocks trading at high relative prices), and small vs. large cap stocks, also varied between decades. Small cap and value stocks outperformed large cap and growth stocks in the 2000s, while the 2010s produced mixed outcomes. Small caps underperformed large caps in the US and emerging markets but outperformed in the developed ex US market. Value underperformed growth in all three market regions. Despite underperforming large cap and growth in the US, small cap and value delivered 11.83% and 11.71%, respectively, for the decade.

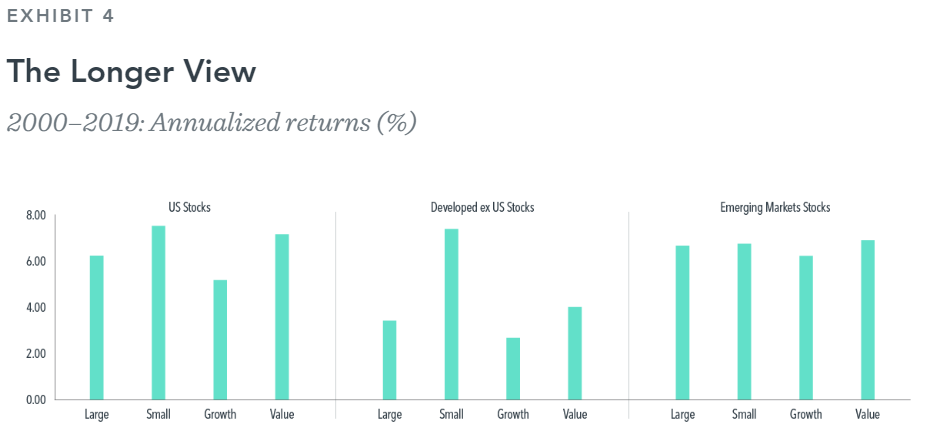

Exhibit 4 shows the cumulative investment experience over both decades, with small cap and value stocks outperforming large cap and growth stocks, respectively, across the US, developed ex US, and emerging markets. The annualized 20-year returns illustrate how diversification can help investors ride out the extremes to pursue a positive longer-term outcome.

Market segment (index representation) as follows: US Stocks—Large Cap (Russell 1000 Index), Small Cap (Russell 2000 Index), Growth (Russell 3000 Growth Index), nValue (Russell 3000 Value Index); Developed ex US Stocks—Large Cap (MSCI World ex USA Index), Small Cap (MSCI World ex USA Small Cap Index), Value (MSCI World ex USA Value Index), Growth (MSCI World ex USA Growth Index); Emerging Markets Stocks—Large Cap (MSCI Emerging Markets Index), Small Cap (MSCI Emerging Markets Small Cap Index), Value (MSCI Emerging Markets Value Index), Growth (MSCI Emerging Markets Growth Index). Index returns are in US dollars, MSCI indices are net of withholding tax on dividends. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2020, all rights reserved. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

Over the past decade, global fixed income also posted returns that may have surprised some investors. In 2010, investors looking at historically low interest rates may have expected rising rates as financial markets and economies recovered from the crisis. But over the decade, short-term rates increased while long-term rates decreased. Realized term premiums were positive, as long-term bonds generally outperformed shorter-term bonds. Realized credit premiums were also positive, as lower-quality bonds generally outperformed higher‑quality bonds.2

Enduring Principles

That brings us to now—January 2020. Stocks and bonds in the US, and in many other developed markets and emerging markets, logged strong returns last year. The US bull market is 10 years old, and current headlines can give investors other reasons to worry about the future—for example, a pushback on globalization, the effects of climate change, the limits of monetary policy, the fate of Brexit, and the vagaries of the 2020 US presidential race. And those are merely the known unknowns. Looking ahead, who can say what the next 10 years will bring? The only certainty is the decade will have its own set of surprises.

Here’s what we can learn from the past decade (and the ones that came before it): Despite all the change and uncertainty, the fundamentals of successful investing endured. Diversify across markets and asset groups to manage risks and pursue higher expected returns. Stay disciplined and maintain a long-term perspective. Take the daily news with a grain of salt and avoid reactive investment decisions based on fear or anxiety. Don’t try to predict future performance or time the markets. Instead, develop a sensible investment plan based on a strong philosophy—and stick with it.

Investors who follow these principles can have a better financial journey in any decade.

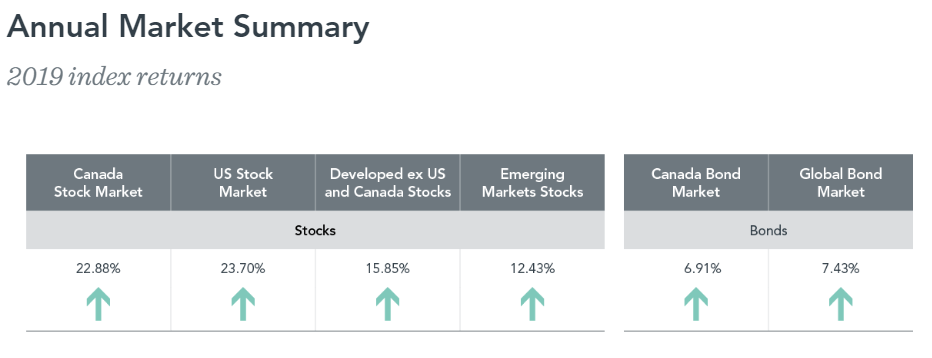

2019 in Numbers

In Canadian dollars. Market segment (index representation) as follows: Canada Stock Market (S&P/TSX Composite Index), US Stock Market (Russell 3000 Index [net of tax]), Developed ex US and Canada Stocks (MSCI EAFE Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Canada Bond Market (Bloomberg Barclays Canadian Aggregate Bond Index), and Global Bond Market (Bloomberg Barclays Global Aggregate Bond Index [hedged to CAD]). S&P/TSX data provided by S&P/TSX. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2020, all rights reserved. Bloomberg Barclays data provided by Bloomberg. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

In Canadian dollars. Market segment (index representation) as follows: Canada Stock Market (S&P/TSX Composite Index), US Stock Market (Russell 3000 Index [net of tax]), Developed ex US and Canada Stocks (MSCI EAFE Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Canada Bond Market (Bloomberg Barclays Canadian Aggregate Bond Index), and Global Bond Market (Bloomberg Barclays Global Aggregate Bond Index [hedged to CAD]). S&P/TSX data provided by S&P/TSX. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2020, all rights reserved. Bloomberg Barclays data provided by Bloomberg. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

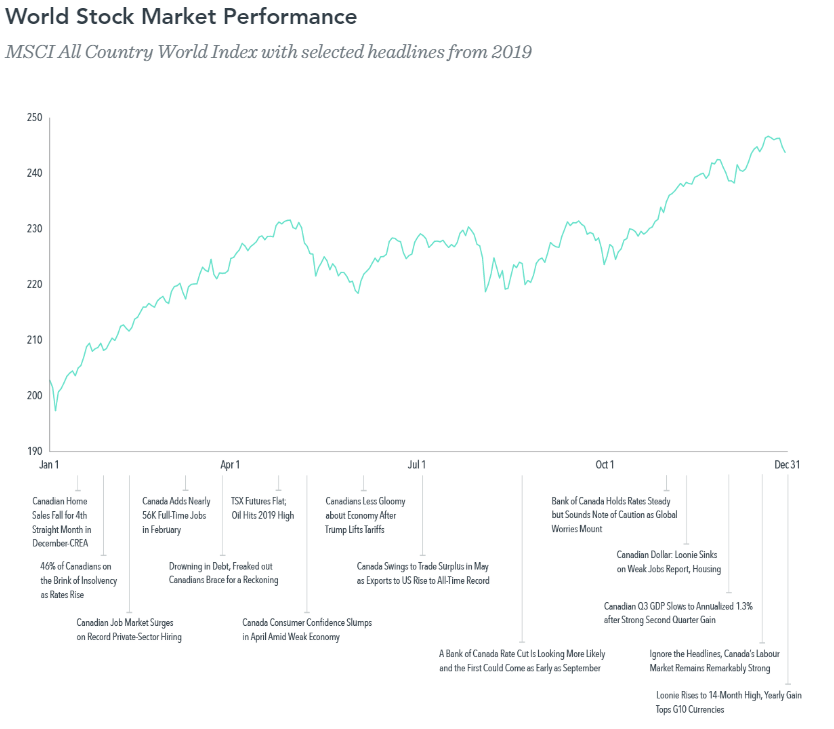

Graph Source: MSCI. In Canadian dollars, net dividends. MSCI data © MSCI 2020, all rights reserved. It is not possible to invest directly in an index. Performance does not reflect the expenses associated with management of an actual portfolio.

*Annualized

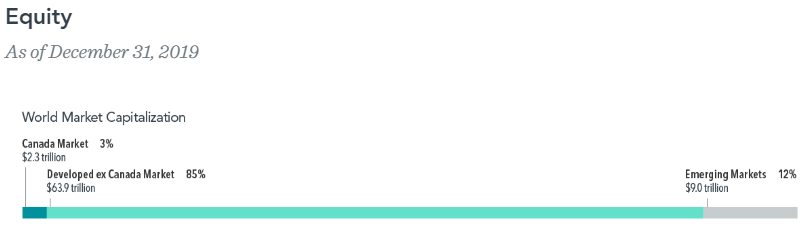

In Canadian dollars. World Market Cap represented by MSCI Canada IMI Index, MSCI World ex Canada IMI Index, and MSCI Emerging Markets IMI Index. MSCI World ex Canada IMI Index is used as the proxy for the developed market. MSCI Canada IMI Index is used as the proxy for the Canada market. MSCI Emerging Markets IMI Index used as the proxy for the emerging market portion of the market. Market segment (index representation) for Canada as follows: Marketwide (S&P/TSX Composite Index), Large Cap (S&P/TSX 60 Index), Small Cap (S&P/TSX Small Cap Index), Value (MSCI Canada Value Index [gross div.]), and Growth (MSCI Canada Growth Index [gross div.]). Market segment (index representation) for US as follows: Large Cap (Russell 1000 Index), Small Cap (Russell 2000 Index), Value (Russell 3000 Value Index), and Growth (Russell 3000 Growth Index). Market segment (index representation) for developed markets ex Canada and US as follows: Large Cap (MSCI EAFE Index), Small Cap (MSCI EAFE Small Cap Index), Value (MSCI EAFE Value Index), and Growth (MSCI EAFE Growth Index). Market segment (index representation) for emerging markets as follows: Large Cap (MSCI Emerging Markets Index), Small Cap (MSCI Emerging Markets Small Cap Index), Value (MSCI Emerging Markets Value Index), and Growth (MSCI Emerging Markets Growth Index). MSCI and Russell index returns are net of withholding tax on dividends except where noted. S&P/TSX data provided by S&P/TSX. Frank Russell Company is source and owner of trademarks, service marks, and copyrights related to Russell Indexes. MSCI data © MSCI 2020, all rights reserved. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio.

*Annualized

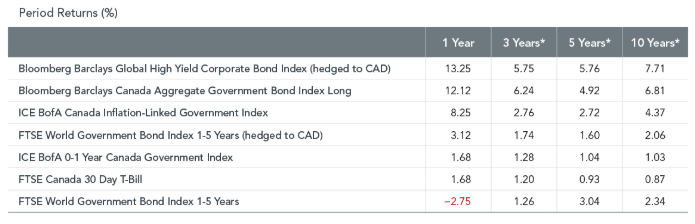

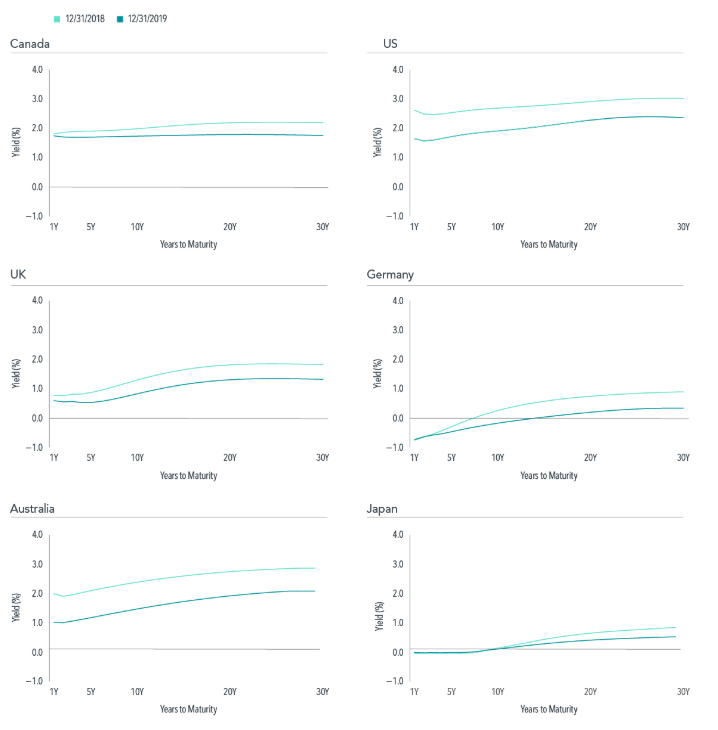

Yield curve source: ICE BofA government yield. ICE BofA index data © 2020 ICE Data Indices, LLC. FTSE fixed income indices © 2020 FTSE Fixed Income LLC, all rights reserved. ICE BofA index data © 2020 ICE Data Indices, LLC. S&P data © 2020 S&P Dow Jones Indices LLC, a division of S&P Global. Bloomberg Barclays data provided by Bloomberg. All rights reserved. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Period returns in Canadian dollars.

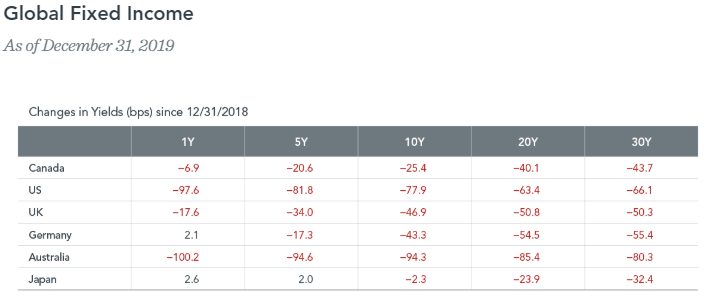

One basis point equals 0.01%. Source: ICE BofA government yield. ICE BofA index data © 2020 ICE Data Indices, LLC.

FOOTNOTES

1“Bull Market Shows Signs of Aging,” The Wall Street Journal, December 7, 2009.

2 Bloomberg Barclays Indices