Good Afternoon,

Equity markets were relatively flat on the week. The S&P 500 flirted with a new high for three days, finally made it on Thursday, and then promptly gave it back. It was a difficult week for politicians in Canada with articles bringing up outdoor dinners, the Keystone XL cancellation, the C-10 censorship bill, and Ontario continuing to be criticized for keeping schools closed while the rest of the country shows that in-person learning and declining case counts are possible. Many parents in Ontario are outraged as they see Covid rates in Ontario are still higher than in Quebec and B.C. where schools have largely remained open. One member of Ontario’s Science Table this week even admitted that school closures are more about getting adults to stay at home than they are about the transmission of COVID-19 within the classroom:

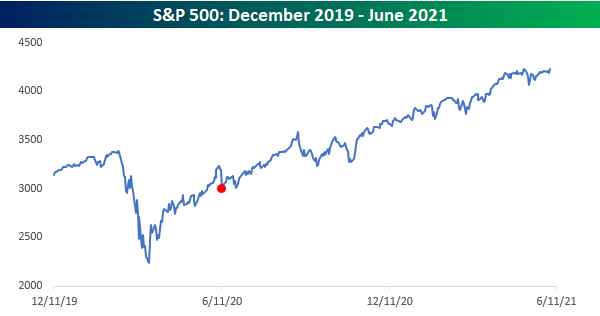

The worst June 11th for the US stock market in history was exactly a year ago today when the S&P 500 fell close to 6% and every stock in the S&P 500 was down on the day except a Grocery chain, Kroger. Last June 11th no doubt caused a lot of stress for investors at the time, but looking at the move from a longer-term perspective, it was little more than a speed bump on the road to recovery.

In contrast to last year’s June 11th plunge, the best June 11th for US stocks was more than 80 years ago in 1940. Europe was already embroiled in war and things escalated when Italy joined the war effort of the Germans by declaring war on the French and attacking a British naval base in Malta. Despite the escalation of conflict, the market confidently rallied anyway. The reason? For starters, it was coming off a major plunge in May following the German attack of France and other areas of Western Europe. Besides being extremely oversold, another catalyst for the rally was an address by President Roosevelt at the University of Virginia commencement which has come to be known as the “Knife in the Back” speech. In that speech, FDR ditched his prepared comments and instead called for an end to the United States’ isolationism in response to Italy’s actions. He commented that “On this tenth day of June, 1940, the hand that held the dagger has struck it into the back of its neighbor.”

Coronavirus update

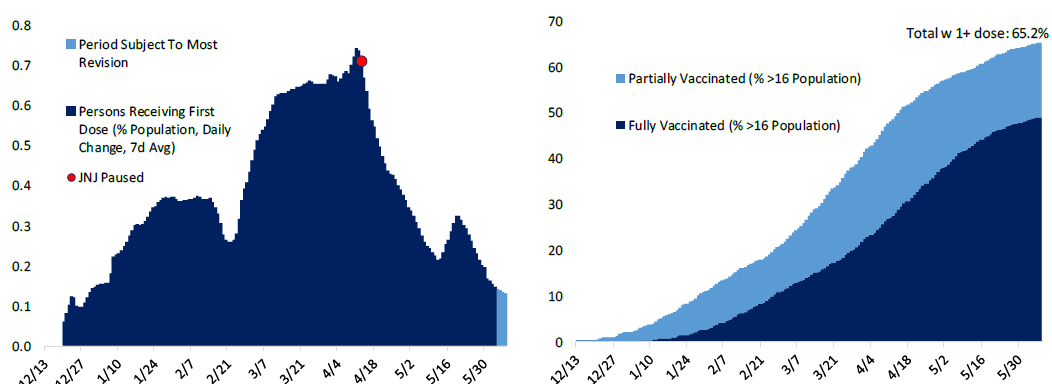

Canada continues to see a decline in daily virus infections with the 7-day average now down to 1510, far below the April high of 8700. Alberta has been notably strong with only 178 cases reported yesterday and the 7-day average now down to 217 from a peak of over 2000. 63.5% of Canadians have now received a single dose of a Covid vaccine and over 10% have two doses. 74% of Canadian adults (18+) now have a first dose. In the last 14 days in Alberta 96% of cases were unvaccinated or within 14 days of their first dose, with 93% of hospitalizations and 88% of deaths also falling within those parameters. I got my second Pfizer jab yesterday and I’m feeling great today, no side effects so far!

Despite widespread first dose uptake, the UK is seeing an acceleration in COVID case counts that has sent new daily cases to 86 per million over the past 7 days, more than triple the 23.5 per million new case rate on May 21st. The good news is that virtually all of the increase in new cases is coming from younger age groups, with no material increase in the case rates for the 65+ category and huge jumps for those under 30 that are much less-vaccinated. This is just more evidence that vaccines are important and any population not vaccinated will remain at risk from the disease indefinitely.

The controversial U.S. decision to temporarily suspend JNJ vaccine administrations earlier this year, as shown below, led to a reversal of accelerating vaccine dose rollouts across demographics, and may end up being the biggest single factor that prevents the US from vaccinating at least 80% of its population. The FDA was not necessarily acting in bad faith or making an obvious error but is being forced to balance competing interests under conditions of uncertainty; it may be that there is no good decision to be made in those circumstances. Having fewer unvaccinated arms available was eventually going to slow down the pace of vaccinations but the change in vaccination rates after the JNJ pause is remarkable.

Inflation

"Inflation hasn't ruined everything. A dime can still be used as a screwdriver." - H. Jackson Brown, Jr.

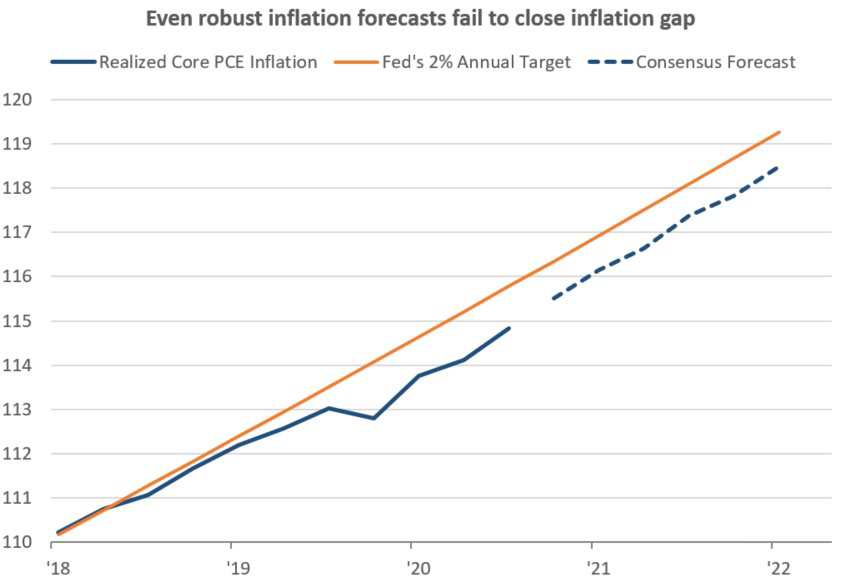

Tuesday, investors who still read a physical newspaper were greeted with some interesting headlines related to inflation. Right below the fold on the front page of the Wall Street Journal, they saw "Commodity Prices Skyrocket, Adding to Inflation Fears". Then on the front page of the Markets section right at the top was the headline "Traders Bet on Return of $100 Oil". With headlines like that and a 5% CPI report posted on Thursday, weakness in the Bond market would be a safe assumption. Not so fast. While the yield on the 10-year US Treasury was an already low 1.57% when the Journal came off the presses, ever since then, it has done nothing but go down. In fact, as of this morning, the yield dropped below 1.5% and is on pace for the lowest closing yield in over three months. This is particularly relevant as the bond market has historically been the best predictor of future inflation, with higher interest rates often leading periods of future inflation growth.

It’s also important to recall that inflation is typically measured on year over year terms and looking back over the last couple years inflation has been so low that higher year over year inflation rates are now almost inevitable (see chart below). Many of the components causing higher inflation in the latest report are clearly Covid related and could be transitory, they include auto sales and rentals (people avoiding public transit), lodging airfares and recreation (these were very cheap a year ago), as well as household goods and education & communication services (in demand during a pandemic). I have attached a recent RBC presentation on the outlook for inflation for anyone who is interested. An audio commentary summarizing the presentation is also available on our website: https://ca.rbcwealthmanagement.com/andrew.king/blog

https://ca.rbcwealthmanagement.com/andrew.king/blog

Best Regards,

Andy, Sacha and Mike

What we were reading this week:

If you aren’t familiar with Bill C-10 I think it’s the biggest non-Covid issue facing Canadians right now. The thought of internet and social media censorship in a democracy is frightening:

https://globalnews.ca/news/7927985/bill-c-10-free-speech-social-media-questions/

https://globalnews.ca/news/7862794/bill-c-10-social-media-free-speech-broadcasting-act/

https://www.spiked-online.com/2021/06/04/why-i-spoke-out-against-lockdowns/

https://www.wsj.com/articles/the-science-suggests-a-wuhan-lab-leak-11622995184

https://financialpost.com/opinion/matthew-lau-ontarios-default-position-is-now-government-control

https://golf.com/instruction/golfer-ditched-worst-advice-golf/