Key points

- Historically, elections that significantly impacted a country’s economy and financial markets were those where the elected government implemented a sweeping structural reform programme, modified fiscal or monetary policies, or refashioned international relations.

- In emerging markets, we believe the outcomes of this year’s elections will have important implications for ongoing reforms and economic stability. For some, how the elections play out may accelerate the breakdown of the post-Cold War world order.

- In developed markets, at this juncture a centrist government appears likely, in our view, to win the next UK general election, while voting for the European Parliament may give populist nationalists a greater voice, further threatening the cohesion of the EU.

Elections as game changers?

Every now and then, elections have deep, long-term implications for economies and financial markets. In particular, those where an elected government has promised wide-ranging economic changes, such as:

- The 1979 UK election of Prime Minister Margaret Thatcher brought privatization of state-owned companies, financial system deregulation, and labour market reform that initially worsened the UK’s long economic downturn but ultimately reshaped its economic structure.

- Brazil’s 1994 election led to a transformation of monetary policy orthodoxy for its central bank, which helped tame the hyperinflation that had gripped the country for years.

The subsequent improvement in both economies paved the way for lasting bull markets in their respective domestic equity markets.

We’ve also seen how elections have upended international relations, be it foreign policy or trade:

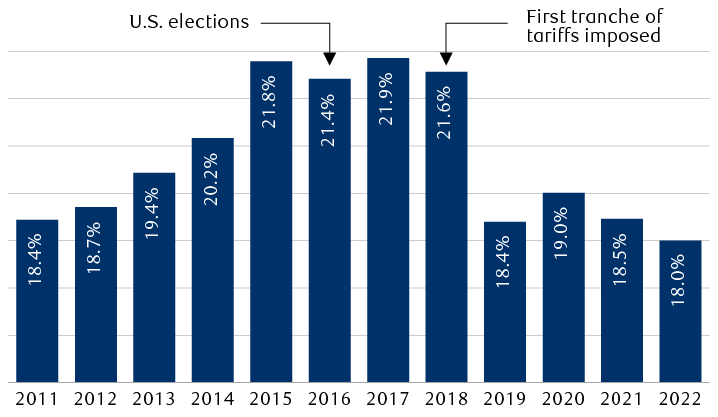

- After the election of Donald Trump as U.S. president in 2016, his administration imposed a series of tariffs starting in 2018 that kicked off a trade war with China and contributed to the fracturing of the post-Cold War world order. A frostier geopolitical backdrop, among other factors, may have contributed to the underperformance of Chinese equities relative to U.S. equities since then.

After tariffs were imposed, the contribution of imports from China fell

U.S. imports from China as a percentage of total

Bar chart showing U.S. imports from China as a percentage of total imports for the period of 2011 through 2022. In 2011, U.S. imports from China represented 18.4 percent of the total. The percentage peaked at 21.9 percent in 2017 and has been falling since. By 2022, U.S. imports from China represented 18 percent of the total, a smaller contribution than in 2011.

Source - World Bank

Campaign promises of change, though, do not mean an election outcome will be momentous enough to fundamentally alter the economy and markets. Governments typically need the ability to implement these changes via a legislative majority. It’s far easier to accomplish this in countries with only two major political parties, such as the U.S., the UK, and India.

Countries where several parties vie for the electorate often end up with coalition governments, the norm for many European countries. To successfully and efficiently implement changes, it’s best if the coalition shares common political ideologies. Coalitions that hold divergent views and/or are cobbled together mainly to topple the incumbent tend to be unstable and have a poor track record at bringing about meaningful changes.

Absent the means to effect change, grandiose proposals can be watered down or never become reality:

- Javier Milei, the self-described “anarcho-capitalist” elected president of Argentina in November 2023, is a case in point. He promised drastic economic measures including cutting public spending by 15 percent, abolishing the country’s central bank, and making the U.S. dollar the country’s legal currency. But his party only controls about a quarter of the seats in each house of Congress, making it difficult to pass legislation.

Will the 2024 election cycle herald big changes?

Few of the 2024 elections are likely to be as pivotal as the ones outlined above—after all, many countries have already introduced sweeping reform programmes, and most central banks are now independent and have demonstrated their usefulness by taking dramatic action to lower inflation. Nevertheless, how this year’s elections shake out will have crucial ramifications for ongoing reform programmes, economic stability, and international relations, in our view.

The ones to watch

Emerging markets

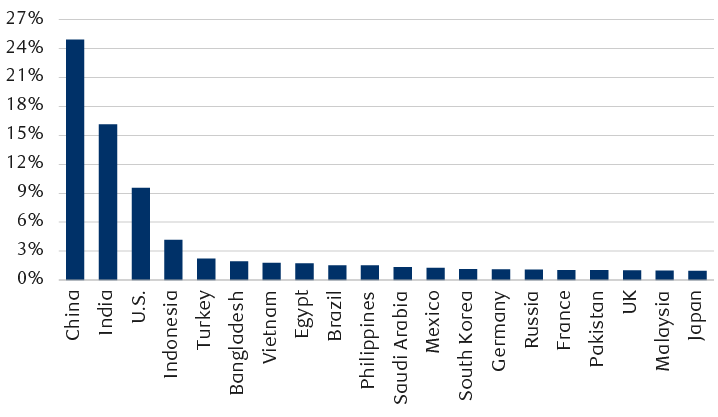

According to the IMF, emerging economies will generate more than 60 percent of global GDP growth over the next five years. So, we think it is more important than ever to understand how some of this year’s elections may influence emerging economies’ prospects.

China and India are anticipated to be the main GDP growth drivers over the next five years

Share of world GDP growth from 2023 to 2028

Bar chart showing various countries’ share of world GDP growth from 2023 to 2028. China will be the largest contributor, bringing close to a quarter of world GDP growth over the period, with India's share at 16%. This compares to the U.S. contributing just under 10% of world GDP growth. Overall, adding up all the contributions from emerging economies, they will contribute together more than 60% of world GDP growth between 2023 and 2028.

Note: Based on IMF forecast from 2023 to 2028.

Source - International Monetary Fund (IMF) World Economic Outlook October 2023, Macrobond, RBC Global Asset Management

Many countries, such as Indonesia and India, have introduced reforms relatively recently, but we think they still have much to do. Whether elected governments remain committed to such efforts will likely determine if countries can maintain a growth trajectory, in our opinion.

For some nations, such as Pakistan and Sri Lanka, which recently signed financing agreements with the International Monetary Fund (IMF), we believe maintaining economic orthodoxy is key to promoting economic stability.

Finally, electoral results in Taiwan, Bangladesh, Mexico, and Venezuela will have consequences for international relations.

Below, we focus on two countries, India, given its increasingly large role in the global economy, and South Africa, as the ruling African National Congress potentially losing its majority could cause ripples in financial markets.

India – Will it remain the darling of EM investors?

India is likely to be the second-largest contributor to global economic growth after China over the next five years, and it has gradually opened its economy to foreign investors. Meanwhile, Indian government bonds have recently been incorporated into the Emerging Markets Global Diversified Bond Index, a key benchmark.

Polina Kurdyavko, head of RBC BlueBay Emerging Markets, attributes India’s newfound role in the global economy to several factors:

- The country’s relative neutrality amidst global conflicts; India is a member of both the BRICS bloc (along with Brazil, Russia, China, and South Africa) and the U.S.-led Quadrilateral Security Dialogue, commonly known as the “Quad,” along with Japan and Australia.

- Relative political stability.

- Proximity to the Middle East, as well as improved relations with Saudi Arabia, the United Arab Emirates, and Egypt, all of which contributed to helping India become a new regional power.

- High levels of employment with 70 percent of the population working and labour costs now lower than those in China. This enables India to offer solutions to countries facing recent workforce shortages by increasing its manufacturing capacity, easing supply chain bottlenecks, and bridging labour gaps.

Between April and June, as many as 945 million eligible Indian voters will head to the polls, the largest-ever democratic event. The central government will be formed by the party—or parties—that achieves a majority in the 543-seat lower house of parliament (the Lok Sabha). The election appears likely to provide the country with leadership continuity.

Prime Minister Narendra Modi enjoys an approval rating of 77 percent, the highest level of any democratically elected leader in the world despite having already served two terms, according to Morning Consult, a market research firm.

Modi’s humble background and economic track record are appealing to the electorate. His government oversaw a wide-ranging supply side reform programme which included:

- A broad bank recapitalization package and a new bankruptcy code (in Modi’s first term).

- Labour reforms and a new digital identification system that enabled digital payments and data-management platforms (in the second term). These initiatives gave most Indians access to public services and facilitated the receipt of popular government cash transfers.

Underpinned by the reforms, India’s economy has grown at enviable rates of close to six percent annually on average during his tenure. The stock market has similarly been on an uptrend, gaining more than 200 percent since his election in 2014.

Additional gradual structural reforms are needed for India to maintain its economic momentum, in our opinion. Job creation remains low, with a large percentage of the population underemployed. Education levels are still inadequate for an aspiring economic power.

We believe it’s important that a stable government with a working parliamentary majority emerges from the election, be it a single-party majority or a sturdy coalition. This would heighten the prospects that reforms face few obstacles in the Lok Sabha, are implemented efficiently, and have a greater likelihood of resulting in healthy economic growth over the coming years. Failing this, we think foreign investor confidence might be shaken and could result in capital outflows.

South Africa – Unsolid ground

With its general election approaching in May, South Africa is facing many challenges, and we think the outcome could generate more turmoil. In particular, with the spread on South African 10-year government bonds versus U.S. Treasuries reaching a 20-year high in 2023, we are keeping an eye on this election. An outcome that leads to abandoning fiscal and monetary rectitude could rattle financial markets, in our view.

Following a crippling energy crisis, the ruling ANC under President Cyril Ramaphosa could lose its majority for the first time in 27 years. In 2023, the state-owned power utility was unable to supply close to half of its potential generation capacity to consumers, setting off blackouts that continue to plague the country.

Should the ANC form a coalition with the left-wing Economic Freedom Fighters, it could pressure the South African Reserve Bank, one of the few central banks which is not independent, to abandon its arduous fight against inflation. Moreover, what we believe is much-needed fiscal consolidation to rein in budget deficits would be less likely to be implemented. With both monetary and fiscal policy loose, concerns regarding national sovereign debt risks, already high, could mount and spreads could widen further, setting off jitters across financial markets.

South Africa’s debt levels soared from less than 30 percent of GDP before the global financial crisis to 70 percent of late. This debt load is even higher once state-owned enterprises are included.

Developed markets

Among the developed economies (apart from the U.S.), the UK general election and European parliamentary elections should attract the most attention. Having flirted with populist and nationalist sentiment since the Brexit referendum, we think the UK seems poised to embrace a more centrist government.

UK – Winds of change?

In the UK, polls have been decidedly pointing to a Labour government, with the party sustaining a 20 percent lead over the incumbent Conservatives for more than a year.

Labour leader Sir Keir Starmer has made much of wanting to return the UK economy to a growth path. Still, with fiscal and monetary policy being tight, any new government will have little room to maneuver, in our view, given the UK deficit is running at over five percent of GDP and the Bank of England’s ongoing fight against inflation. If elected, one area Starmer could tackle is the relationship with the EU, which continues to be the country’s largest trading partner.

Over the past few months, the EU has shown willingness to engage with the UK in a more flexible manner—that is, without requiring discussions about rejoining the single market or the EU Customs Union. In July 2023, cognizant that the geopolitical context had darkened substantially over the past few years, EU officials raised the idea of a formal collaboration on global issues with its former member.

As the engineer of Brexit, the Conservative government declined that offer. But a Labour government may well be more open to greater collaboration in areas of mutual interest. For example, agreements such as one covering freedom of movement between the UK and EU could be a boon to the struggling UK economy and stock market, which has suffered significant outflows since the Brexit referendum.

European Parliament elections – Louder radical right and anti-establishment populist voices

Over three days from June 6, 450 million Europeans will elect 750 representatives for the bloc’s next Parliament. The European Parliament’s main role is to consider budgets and legal proposals made by the European Commission in Brussels.

At stake are Brussels’ support for Ukraine, the bloc’s ambitious measures to tackle climate change (including targets for cutting carbon emissions), and immigration. The extent of Brussels’ involvement in national economic, fiscal, and regulatory policies is also in the balance.

The European Council on Foreign Relations (ECFR), a think tank, suggests a more populist, right-leaning European Parliament is likely to emerge from the elections, based on recent polls and its own assessment of potential coalitions. Such an outcome may hinder the passing of legislation necessary to implement the next phase of the European Green Deal and lead to a harder line on migration, while support for Ukraine and EU enlargement may soften over time. Overall, this scenario could amplify dissent within the bloc.

A right-leaning European Parliament would also influence national governments’ domestic politics. For instance, if citizens in a particular country were to vote in the European Parliament elections for a party that does not support the Green Deal agenda, we think it would very likely affect the position that country’s government may feel able to take when formulating its own national policies on curbing carbon emissions.

Meanwhile, the outcome of the U.S. election will also influence the bloc’s policies, economy, and industries. If he returns to the White House, Trump plans to impose a broad minimum 10 percent tariff on all imported goods, as well as to likely retaliate against European digital services taxes that target U.S. tech leaders. It would also mean Europe’s ally would be less engaged. Some European leaders, such as French President Emmanuel Macron, may increase calls for the Continent to depend less on America for defense. However, the rise of populist, anti-establishment parties, some of which are more sympathetic towards Russia, would make this aim more difficult to achieve, in our view.

In a nutshell

The results from this year of elections will shape the economic landscape for a number of nations, in our opinion. Where new governments put reform programmes at risk, financial market volatility may increase. Where voters embrace reform efforts, those countries may be able to continue on a growth path. Elsewhere, anti-establishment voices holding more sway may result in increased difficulty in effectively setting and implementing policies.

Overall, we believe the breakdown of the post-Cold War world order is likely to continue. Much will be decided by an outside factor, in our view, as the outcome of the U.S. election will also be a key driver and could shift prospects significantly for many nations.