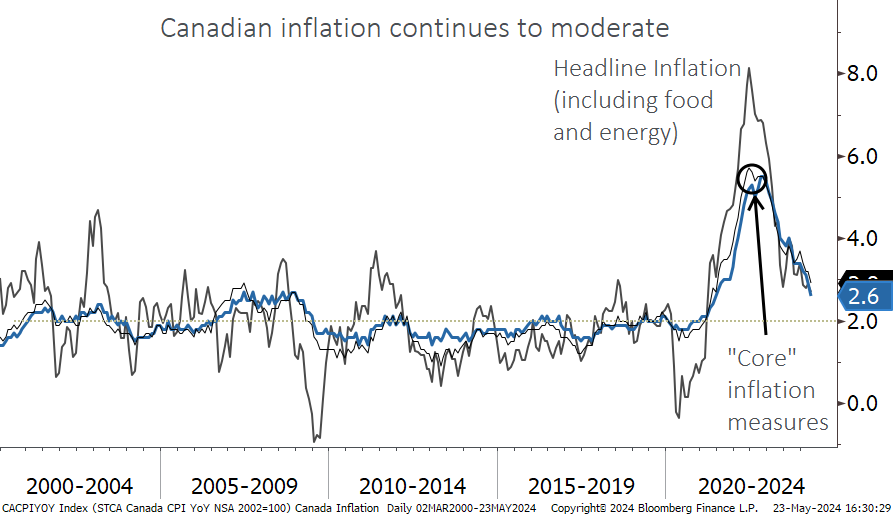

- Canadian inflation indicators continue to moderate, opening up the door for the Bank of Canada to offer some interest rate relief.

- Inflation has been trending lower all year and in contrast to the U.S., the pace of decline has not flattened out.

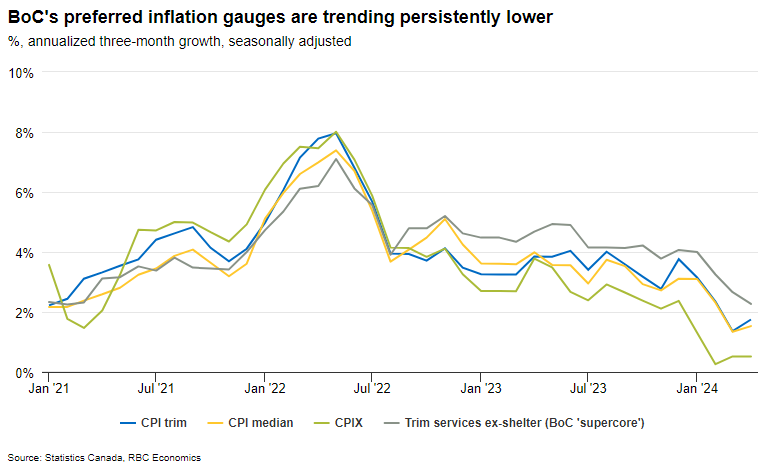

- The Bank of Canada’s preferred inflation measures are closing in on 2% when looked at on a 3-month basis.

- Markets are pricing in a 60% chance of a rate cut in June and a cut by July is fully priced in.

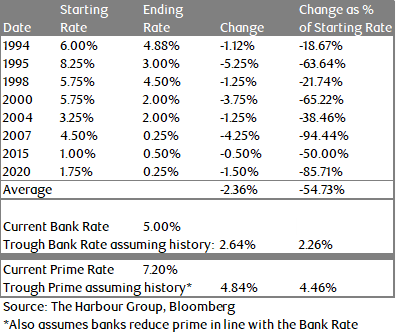

- Historically, rate cutting cycles tend to see multiple rate cuts as opposed to small tweaks.

- With markets already expecting rate cuts, the greatest impact may well be if the Bank of Canada accelerates the pace, leading to lower bond yields and making dividend paying stocks more attractive.

This past week brought the most recent update on Canadian inflation, and we are happy to report that the disinflationary trend continues. Both the headline inflation figure, and the Bank of Canada’s preferred indicators which strip out the most volatile components trended lower on the month and are now well within the Bank’s 1-3% inflation target range.

Door now wide open for rate cuts…

When looked at on a three-month annualized basis in order to better isolate recent trends, the news is even better, with three of four indicators below 2%. It is this development which has given investors confidence that the Bank of Canada is close to initiating an interest rate cutting cycle. Bond markets are pricing in a 60% chance of a rate cut in June, with a 100% chance priced in for July. Barring something unforeseen in the economic data, we will likely see a more benign interest rate environment begin to take shape.

… but how many will we see?

As of today, markets are pricing in about two rate cuts by the end of this year, and the expectation is currently that the Bank of Canada policy rate will bottom out at about 3.25% in two years. RBC’s forecast is for the policy rate to hit 3% by the third quarter of 2025. When we look at history, Bank of Canada easing cycles can be measured two ways: How much did they cut rates by measured in percentage terms, and how much did they cut as a proportion of the peak interest rate.

In percentage terms, the average drop has been 2.36%, while the trough interest rate has generally been about 55% lower than the starting rate. Applying those two methodologies to today’s 5% policy rate would suggest this easing cycle takes rates to the 2.5% range if it follows historical averages. Provided banks keep the differential between the prime interest rate and the policy rate the same, this would suggest prime could fall from 7.2% currently to somewhere in the mid-4% range over time.

How will markets react?

As we know, markets are forward looking mechanisms, so in theory the bond and stock markets already reflect an eventual interest rate decline. As mentioned above, the expected changes in the Bank of Canada rate are fairly muted. If we do see a rate cutting experience more in line with history we would expect bond yields to drop further, boosting returns for bonds, especially those with longer terms to maturity. As the competition posed by bond yields diminishes, we would expect investors to gravitate back toward beleaguered dividend paying stocks which we see having upside potential in excess of the broad bond market.

The Harbour Group

416-842-2300

Putting you first, every time, to help you navigate the complexities of managing your wealth. All of our team members, all of our resources, all of our collective insight: ALL FOR ONE: YOU™.

The information contained herein has been obtained from sources believed to be reliable at the time obtained but neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers can guarantee its accuracy or completeness. This report is not and under no circumstances is to be construed as an offer to sell or the solicitation of an offer to buy any securities. This report is furnished on the basis and understanding that neither RBC Dominion Securities Inc. nor its employees, agents, or information suppliers is to be under any responsibility or liability whatsoever in respect thereof. The inventories of RBC Dominion Securities Inc. may from time to time include securities mentioned herein. RBC Dominion Securities Inc. and its affiliates may have an investment banking or other relationship with some or all of the issuers mentioned herein and may trade in any of the securities mentioned herein either for their own account or the accounts of their customers. RBC Dominion Securities Inc. and its affiliates also may issue options on securities mentioned herein and may trade in options issued by others. Accordingly, RBC Dominion Securities Inc. or its affiliates may at any time have a long or short position in any such security or option thereon. Mutual funds are sold by RBC Dominion Securities Inc. There may be commissions, trailing commissions, management fees and expenses associated with mutual fund investments. Read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. RBC Dominion Securities Inc.* and Royal Bank of Canada are separate corporate entities which are affiliated. *Member CIPF. ®Registered Trademark of Royal Bank of Canada. Used under licence. RBC Dominion Securities is a registered trademark of Royal Bank of Canada. Used under licence. ©Copyright 2019. All rights reserved.